Skip to content

Skip to content

Becoming a parent has turned me into an involuntary firefighter.

I don’t get a cool hat, or get to drive a big red truck, but I do get woken up in the middle of the night to deal with pee-soaked bedsheets, or having to deal with a mid-day meltdown in the middle of the grocery store, or hearing the sound of glass shattering as another dish gets broken.

I used to be able to leisurely stroll to a coffee shop or library and just sit there for hours, uninterrupted, typing away on my laptop. Those days are over. Now, there are so many half-finished emails and incoherent texts that I’m sure my friends and family think I’ve had a stroke. Nope, no stroke. That would be my son stealing my phone again and running around our apartment sending poop emojis to my mom.

Going from a jet-setting laptop warrior digital nomad to an exhausted parent constantly fighting fires has made me gain a whole new respect for parents everywhere. So to all the tired parents reading this: I see you, I hear you, I totally get it now.

And I totally get why it’s so hard for parents, especially those with young children, to think about their finances. Who has time for spreadsheets when you haven’t slept or had a shower for the past week?

That’s why in our soon-to-be-released book Parent Like a Millionaire (Without Being One), we encourage the reader not to think about FIRE as a giant lofty goal to quit your job, but rather a series of small, bite-size tasks that anyone can do during the little one’s naps.

Start Small

We never think of FIRE in terms of deprivation, but rather a more efficient way of spending your money. In other words, how do we get the same results while keeping more of your hard-earned cash?

Let’s take a relatively small expense that every new parent has to deal with: diapers.

Disposable diapers cost varies, but right now we’re spending about $40 a month for our 2 year old. $40 a month x 12 = $480 a year.

$480 a year may not be a ton of money, but how would you like to make that free instead?

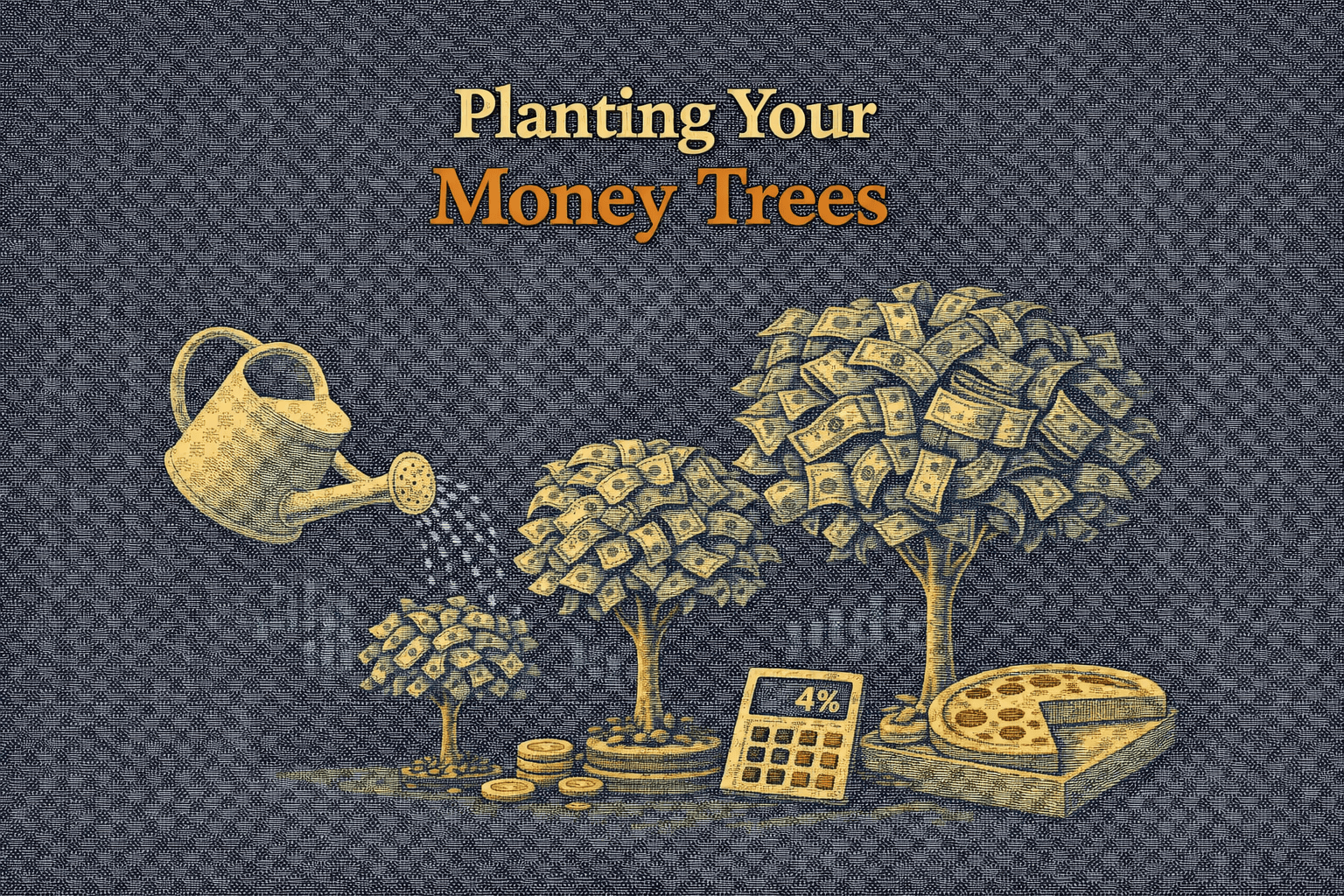

To do this, we need to create a passive income stream equal to $40 a month, or $480 a year.

Fortunately, the FIRE movement has taught us how to do this. To create a passive income stream to match this expense, we take our annual expense ($480) and multiply it by 25, as per the 4% rule.

The 4% rule was originally meant to calculate retirement portfolios, but why not any other expense? Diapers are just like any reoccurring expense, and we know from retirement planning that if you invest 25 times that annual expense amount, you can withdraw the dividends, interest, and a little bit of capital gains to equal 4% of that initial investment, and statistically your investment will never be depleted.

It’s like planting an orange tree in an orchard (your initial investment), and after every year you harvest the oranges while keeping the original tree intact.

So, to create our money tree, it will cost $480 x 25 = $12,000.

Now, $12,000 sounds like a lot of money, especially compared to the diaper’s cost of $480 a year, but there are a few things to keep in mind here:

First of all, the $12,000 isn’t a cost like the diapers are. You’re not spending $12,000, you’re investing it. You’re planting your money tree, and after it starts to bear fruit in the form of dividends, interest, and harvested capital gains, its pays for your diapers going forward. You’ve essentially planted a diaper tree.

Secondly, the money you were spending on diapers (that $480 a year) is now freed up and can be spent on something else. You could put that money towards toys, formula, or whatever else you need. You could even put that money towards planting another money tree, if you want!

And finally, don’t forget that even though babies only need diapers for the first 2-4 years of their lives, your money tree keeps producing forever. After that last nappy is used up, you have a decision to make. What should you do with your money tree? Because you only harvested the fruit without damaging the tree, your initial investment is still there, and may have even grown in value. You could sell it off and cash out your investment. You could redirect that passive income towards another expense, like toys. Or you could merge that money tree with another one, and have it work towards an even bigger expense, like college savings, a new car, or even early retirement!

Subscribe and Win

Here’s another hack that you can use to get your first money tree even faster.

If you direct your diaper orders through an online retailer like Amazon or Walmart, they offer a subscription option in which you sign up for ongoing deliveries, and in exchange you get a discount. Right now, both are offering up to 20%.

20% off $40 a month yields savings of $8 a month. That may not sound like a lot, but let’s see the impact that this move will have on the price of your diaper tree.

After the discount, your $40 diapers will cost $32 a month. $32 a month is $384 a year.

To create a passive income stream worth $384 a year, it will cost $384 x 25 = $9600.

Compared to the original cost of $12,000, this means you can plant your money tree for $2,400 less than before!

And the best part? These changes are completely invisible from your child’s perspective. Your baby is still using the same brand of diapers as before, only now they’re being paid for passively by a money tree rather than out of their parents’ pocket. About the only thing they might notice is that their parents seem happier and more relaxed than before because they’ve done something clever.

Stop Fighting Fires and Start Planting Trees

Parenting can often feel like putting out a series of fires, only to collapse into bed exhausted so you can wake up and do it all over again.

Having been down this particular rabbit hole (what day is it again?) many times, I know how easy it is to fall into the trap of focusing on the immediate emergencies rather than invest in long-term solutions.

But by focusing on small wins and financially automating certain tasks, like buying diapers, you will free up a little bit of your mental and financial bandwidth. When you’re a parent, every minute and every dollar matters, and when you take something off your plate, you can spend that time and money towards something more worthwhile, like focusing on your relationship with your spouse, or even just taking a nap.

So parents: Stop fighting fires and start planting money trees.

Thanks for your hhhhhhhhhhhhhhhhgggggggggggggbgggggggs

1112345654=567 89090–

…And that was my son grabbing my laptop. Again. Le sigh.

Upcoming Webinar

Your Salary Has a Ceiling. Your Rental Income Doesn’t.

I spent years perfecting my ability to generate RVUs. Got really good at it, too. And then one day I did the math on what another decade of that grind would actually buy me, and the answer was… more of the same.

That realization stung.

Here’s what nobody told us in residency: a physician’s W-2 income is a depreciating asset. Your body gets older. Your patience wears thinner. The reimbursement environment gets worse. Meanwhile, a rental property you bought in 2024 keeps collecting rent checks whether you showed up to clinic or not.

That’s cash flow. And it hits different when you understand what it really means for a doctor’s life.

Why I Got Serious About Real Estate

I’ll be honest. I was skeptical. I’d heard the “passive income” pitch from every financial guru with a ring light and a podcast. But when I started looking at what physicians who actually retired early had in common, rental real estate kept showing up. Not crypto. Not options trading. Not some complicated insurance product their “advisor” sold them. Rental properties.

The math is surprisingly clean. You buy a property that generates rent. You subtract your mortgage, taxes, insurance, management, and maintenance. What’s left is yours. Every month. Without charting a single note.

And the tax benefits? They’re almost unfair. Depreciation alone can shelter huge chunks of your clinical income. Pair that with cost segregation and you’re looking at legal write-offs that make your accountant grin.

So Why Do Most Doctors Never Pull the Trigger?

Fear. Time. Confusion about where to start.

I get it. You didn’t go to medical school to become a landlord. You barely have time to eat lunch between patients, let alone analyze duplexes in Memphis.That’s exactly why I’m co-hosting a free webinar with Dr. Kenji Asakura from Semi-Retired MD. Kenji built the Zero to Freedom course after watching too many brilliant physicians work themselves into burnout with zero financial options beyond “keep going.” Over 4,500 doctors have gone through his program. Some bought their first rental property before they even finished the seven weeks.

The webinar covers how one cash-flowing rental can generate six figures in year one, how real estate slashes your tax bill (legally, obviously), and how to buy smart deals regardless of what interest rates or the economy are doing.

You don’t need millions to start. You don’t need landlord experience. You need a calculator, a proven process, and about two hours a week.

This Isn’t About Quitting Medicine

It’s about making medicine optional. There’s a version of your career where you work because you want to, not because your mortgage demands it. Real estate is how a lot of us are getting there.

Date & Time: Saturday, February 28, 2026, at 3:00 PM ET / 12 PM PT

Save Your Seat: Register Now!

Can’t make it live? Register anyway, and they’ll send you the replay.

See you this Saturday.

Article Link: https://www.millennial-revolution.com/invest/planting-your-money-trees/