Each year, I update this Social Security article, gauging my progress and potential future benefit. Now that the 2025 numbers have been released, it’s time for that update

Several years ago, my earnings history surpassed the second bend point, and additional contributions won’t do all that much for me. Don’t know what a “bend point” is? Don’t worry; you will in a few short minutes, and you’ll be able to determine whether or not you yourself have reached the first and second bend points.

The figures and data that follows have been updated for those who would reach Social Security eligibility in 2025, and the Social Security projection spreadsheet, which you can download for free below and fill in your own data, has been updated with the latest indexing factors.

Note that the results are your projected benefit in today’s dollars (present value). Your future benefit will rise with inflation each year, preserving your spending power.

If the calculator suggests you’ll have a monthly benefit of $2,000 and you’re two to three decades away from collecting, you can assume your benefit by then will roughly double in number, assuming inflation averages something near the historical rate of around 3% over that 20 to 30 year period.

Social Security is something we aspiring retirees don’t spend much time talking about.

While we may notice how much we kick in (a maximum of $21,836 as a self-employed individual in 2025), those of us planning to retire early tend to largely ignore it when calculating safe withdrawal rates and our annual cashflow. If we mention it all, it’s usually with an asterisk because the payday is so far off and somewhat uncertain.

In all likelihood, some money will be there for us. The calculations may be different than they are today, but that’s true anytime we make projections based on current tax code, and that’s something we do a lot.

Based on the latest annual report from the Social Security Board of Trustees, the program is fully funded through 2033, and 79% funded for the long term with many options to address the long term shortfall. Politics will play a role in deciding if that means decreased benefits, an older age at which they’re available, or an increase in the amount of salary subject to Social Security tax.

While we don’t know which way it will go, and it’s quite alright to plan as if it doesn’t exist (better safe than sorry), the reality is that Social Security will quite likely be a benefit to many of us in the latter portion of our retirement.

You may be retired and living without it for a decade or two (or even three), but I expect there will be something to collect when you’re in your sixties (or age 70 or even higher if the rules change).

There are some retirees, though, who should not plan on Social Security income.

If you earned your money outside the U.S. and did not pay into the system, you’re out. If you failed to earn income for 10 years (40 three-month quarters of at least an inflation-adjusted $1,510 income (in 2022 dollars)), you’re not eligible. However, non-qualifying spouses married to someone who qualifies for Social Security can receive half their spouse’s full retirement age (FRA) benefit if taken at their own FRA.

Some government employees participate in an alternative pension system, but do not contribute to Social Security. Without those 40 quarters of contributions, there will be no Social Security benefit.

If you are considering an early retirement, I would strongly encourage you to aim for at least ten years of contributions to the Social Security system. Note that these don’t all necessarily have to be completed prior to pulling the FIRE trigger.

If you don’t have your ten years or 40 quarters in before retiring from your primary profession, you should plan on having at least some reportable income whether from a hobby job or self-employment of some kind until you’ve hit your 40 eligible quarters.

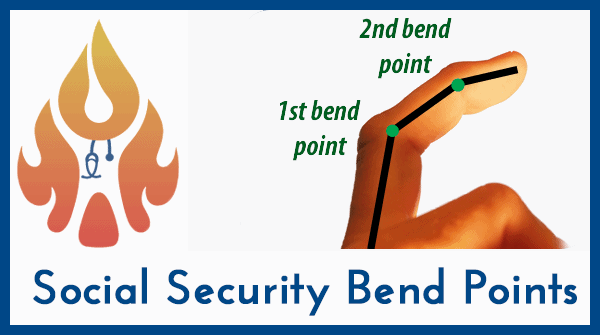

Know the Social Security Bend Points!

What are these bend points? They’re the two points at which you receive diminishing returns in your monthly benefit once you’ve earned a certain amount of money.

The money you’ve contributed over the years is used to calculate your Average Indexed Monthly Earnings (AIME). It’s an inflation-adjusted average of your monthly earnings over your most lucrative 35 years. If you work and contribute for fewer than 35 years, zeroes fill in the blanks.

I’ll have a calculator for your AIME below, but essentially it’s your total inflation-adjusted earnings divided by 420.

What’s the significance of 420? In addition to being one of Elon Musk’s favorite numbers, it’s simply the number of months in 35 years. AIME is important in determining your monthly benefit when taking Social Security at full retirement age.

You get 90% of your AIME up to the first bend point (at an AIME of $1,226 in 2025).

You get 32% of your AIME between the first and second bend points (portion of AIME between $1,226 and $7,391 in 2025)

You get 15% of your AIME beyond the second bend point (AIME above $7,391 in 2025)

For visual learners, let’s use my middle finger as an example. We might as well throw in a couple of joints to accompany all of this 420 talk.

The initial rate of rise in your expected benefit is quite steep until your contributions reach the first bend point (represented by my proximal interphalangeal joint). The slope is less steep between the first and second bend point (my distal interphalangeal joint), and it doesn’t rise all that much beyond the second bend point.

Clearly, building up your AIME to the first bend point at $1,226 is worthwhile. For every dollar contributed up to an AIME of $1,226, you’ll get 90 cents per month when you take Social Security at full retirement age (67 for those of us born after 1959). If you’re earning enough in wages ($176,100 or more in 2025) to contribute the max to Social Security, you’ll hit the first bend point in a few short years.

Earning beyond the first bend point doesn’t do nearly as much for you, but you still get 32 cents for every dollar of AIME between the first bend point and the second at $7,391. Additional years of income between the bend points will make a noticeable difference in your eventual monthly benefit.

Once your Average Indexed Monthly Earnings reach the second bend point at $7,391, you’ll only receive 15 cents per dollar of AIME beyond that. Additional earnings give you vastly diminished returns at this level of AIME. And if you ever have 35 years of maximum contributions, there’s nothing you can do to increase your eventual benefit.

The bend points will increase annually with inflation, as will your AIME as older earnings will be worth more as time goes on. Once you’ve surpassed a bend point, you shouldn’t lose it, because your AIME will increase each year as the bend points grow larger.

Spreadsheet Time

In the sheet below, I’ve entered my information in the white boxes, copied and pasted directly from the ssa.gov website. You can sign in or create an account here to access a lifetime record of your earnings.

You can also find out what your anticipated monthly benefit (known as Primary Insurance Amount or PIA) will be, based on your future salary. The SSA tends to be a year or two behind in recording your earnings, so the number shown here will underestimate your benefit as compared to the downloadable spreadsheet I’ll be demonstrating below.

I’ve created my own calculator that will tell you whether or not you’ve reached the first and second bend point and will estimate your monthly benefit if you were to stop contributing now (or in this case, in 2025).

To extrapolate further if you plan to keep working, each additional year working and contributing the maximum will add about $419 ($176,100 / 420) to your AIME. This assumes your next year working will replace a year of $0 earned and contributed. In other words, the $419 addition to your AIME only happens if you have fewer than 35 years of reported earnings and contribute the maximum in the year that replaces a zero-earnings year.

The calculator featured below should be accurate for those of us born after 1960. The benefits will be slightly higher for our friends born in the 1940s or 1950s — see this table for those adjustments.

My own earnings record is in the spreadsheet below. I had some grocery store and self-employment income before I started making “big money” as a resident in 2002.

From 2006 to 2023, I earned and contributed the max to Social Security, making it 18 years of maximum earnings. I retired for a second time in 2023, so let’s assume my 2024, 2025, and future earnings are zero, and I never contribute to Social Security again.

With a mere 17 additional years of working and making max contributions, I could collect the biggest check possible! As you’ll see below, the marginal benefit of additional contributions is quite small now that I’ve reached the second bend point.

As you can see, with an AIME of $7,791, I’m now well beyond the first bend point of $1,226, and I’m $400 beyond the second bend point that currently exists for 2025 at $7,391.

Since I’ve been tracking and updating this sheet for eight years now, I’ve noticed how that second bend point increases with inflation each year. Also, the credit from prior years’ work becomes more valuable as the index factors for all past years are increased.

In 2017, when I first made these calculations, the second bend point was reached with an AIME of $5,336. In eight years, that second bend point number has increased by $2,055 to $7,391.

Meanwhile, my personal AIME based on my earnings history has nearly doubled from $3,986 to $7,791, That growth has come from a combination of replacing $0 earning years with maximum earning years and from the index factors for prior years growing larger each year.

From here on out, every dollar that my AIME increases will bring me an additional 15 cents in each monthly check. That marginal benefit is less than half of what it was when I was building up to that second bend point.

Note that the primary purpose of this calculator is to show you if you’ve reached the bend points and how close you are if you haven’t yet. The estimate of the future benefit assumes that the program remains unchanged between now and the time you start collecting.

For early retirees, that’s probably many years off and there will likely be changes before you actually collect, but it doesn’t hurt to see what would happen if the program were to remain more or less the same.

Calculate Your Social Security

I’ve created a page for you to enter your own numbers here on the 2025 Social Security Calculator, although it may be easier to simply download the calculator. If you’re not a subscriber, sign up and you’ll receive a link to download. You can opt out of the free subscription at any time.

Feel free to play around with the numbers.

Taking Social Security as soon as it’s available at age 62 results in what’s effectively a 30% penalty. I don’t like 30% penalties. That’s out.

At full retirement age, I get 100% of my calculated benefit. But each year that I hold off nets me an additional 8% per month for life.

Unless I find myself in poor health, the smart money’s on the most money. I plan to delay my benefit until age 70. Currently, waiting to age 70 to collect would give me $46,667 a year in 2025 dollars. That number will rise with inflation each year, even if I stop working and don’t contribute another dime.

The max I could receive from an additional 17 years of work beyond that is $56,328 per year according to the SSA website.

That’s a gain of a measly $568 more per year in Social Security payments for each additional year worked, assuming I make the maximum contribution annually.

You’ve heard of golden handcuffs; these are papier-mâché handcuffs. Know your bend points!

Spousal Social Security Benefits

My wife has done a lot of hard work, but most of it has gone unrecognized by the Social Security Administration. Obviously, the SSA has never had to clean up after me or my kids. But not all hope is lost.

As mentioned earlier, if she doesn’t qualify with 40 quarters, or if her benefit would be less than half of mine, she can file for Social Security at full retirement age (67) and receive half of my FRA benefit as long as I’m still alive, and she would receive my full benefit if I happen to leave this world before her.

Note that she won’t receive half of the benefit I can take at age 70, but rather half of the amount I would have gotten if I had started collecting at age 67, my full retirement age. That works out to be about 40% of my age 70 benefit.

To work out complicated scenarios, I recommend picking up CPA Mike Piper’s excellent resource, simply called Social Security Made Simple.

Mike has also put together a calculator to help you determine an optimal strategy for filing for Social Security benefits as a couple. First, determine your Primary Insurance Amount (PIA) using the spreadsheet, which is the monthly benefit at full retirement age (67 for most readers). My PIA, as you can see, is $3,136.26.

Mr. Piper’s Open Social Security calculator recommends that I file at age 70 and that my wife files early to start collecting at the same time as me, at age 63 and 3 months.

Doing so would give us $60,070 a year while we’re both alive (more than half of our typical annual spending), and that would be cut to $46,664 (my benefit) when one of us passes away.

He calculates the present value lifetime benefit of this strategy (based on actuarial tables) to be $506,273, on average.

If my wife waits a few more years to start collecting when she turns 67, her benefit will be higher, but the calculator figures the chances of me dying prematurely outweighs the extra payments we could receive together.

How will Social Security change between now and my 70th birthday in 2045? I have no idea, but I’ll be sure to track any changes. It’s too much money to simply ignore.

What’s your plan for Social Security? Have you passed the first bend point? The second? Let us know below!

157 thoughts on “Social Security & Early Retirement 2025: Know Your Bend Points!”

Thank you. It was fun to learn about the bend points.

I tried using my own numbers by entering my incomes from the SS website and getting the index factor by entering the year of eligibility in the SS website. I found that the amounts in the spreadsheet were a little larger than the estimates shown in my SS account.

After seeing that there is a difference in total SS taxes that I paid and my employers paid, I deep-dived into it and found that I paid 2% less SS taxes in 2011 and 2012 due to the temporary tax cut. Instead of 6.2%, we only paid 4.2% for two years. After some calculations, I entered my incomes for 2011 and 2012 by multiplying with 0.83871 and I seem to get more accurate numbers that are closer to the estimates in my SS accounts.

But please let me know what you think about this.

Achillea Filipendulina ‘Cloth of Gold’ is a striking perennial known for its vibrant yellow flowers and finely divided, dark green foliage. Here’s a more detailed cultivation guide based on your information:

Cultivation Advice for Achillea Filipendulina ‘Cloth of Gold’:

Sowing Period:

Best sowing times: February to June or September and October.

Sowing Conditions:

Under Glass:

Sow seeds in pots or trays with fine seed compost.

Spread seeds thinly and evenly on the surface.

Cover seeds with a light dusting of compost or vermiculite, as they need light to germinate.

Germination:

Timeframe: 7-14 days.

Temperature: Maintain at 15-20°C (59-68°F) for best germination results.

Seedling Care:

Pricking Out: Once seedlings are large enough to handle, transfer them to individual pots.

Hardening Off: Gradually acclimatize them to outdoor conditions after the risk of frost has passed in the spring.

Transplanting:

In the second season, transplant seedlings to their permanent position.

Spacing: 30-40 cm (12-16 inches) apart.

Soil: Well-drained soil.

Sunlight: Full sun for optimal growth.

Additional Notes:

Tolerates a wide range of growing conditions, including poor soil.

Great for attracting pollinators like bees and butterflies.

Flowers can be used for fresh or dried flower arrangements.

This hardy plant is a great addition to gardens, providing bold, long-lasting color through the summer.

Love your clear explanations, hard work understanding this system, openly sharing spreadsheets and opening my eyes to this aspect of retirement planning (as you mention, silly to assume you’ll get NOTHING from social security). Kinda fun to track.

I am a ways from the 2nd bend point (AIME ~3.1k in 2022).

I was trying to anticipate when I’d reach the 2nd bend point and I have an idea to track this over the years and see how accurate different ‘predictive measures’ are… Would you be able/willing to share the old annual versions of the Excel spreadsheets (e.g. 2017, 2018, 2019 and so on)? Happy to elaborate further but I like to run a projection at the end of each year and it seems to bounce around a bit (some years not changing much, some years changing a surprising amount). I’m curious when my calculations might be become more precise/accurate. In 2020 I predicted I’d hit the second bend point halfway thru 2031; but that projected date is fluctuating more than I had expected when looking at other years’ calculators (you had highlighted this phenomenon seems to work itself out based on “how that second bend point increases with inflation each year. Also, the credit from prior years’ work becomes more valuable as the index factors for all past years are increased”).

I have contributed the max most of my working years as a pharmacist, but I also plan to track my partner’s predictions (unlikely to max SS in current profession, I assume that makes prediction more sporadic/difficult – but would like to test that hypothesis).

No rush whatsoever and if it won’t work out NBD and I’ll download copies in subsequent years.

As you can see I’m in the “boring middle of accumulation” and interested in tracking somewhat esoteric (trivial?) aspects of personal finance. Thank you for all you do!

druginfogeek@gmail.com

I’m starting Social Security next month, and they sent me a letter yesterday noting my benefit. Their benefit amount didn’t match what I had calculated on my own spreadsheet, by about $40 a month (so no big deal but… wanting to understand how things work); I wondered what I had done incorrectly, and found your spreadsheet. But pasting my incomes into your calculator I came up with quite a different result on the sum of 35 years of indexed wages.. As a suggestion: It doesn’t appear that your calculator limits annual earnings to the Social Security maximum capped amount. That would throw the numbers off. My questions:

1. Do you set the index factor to 1 for the years after you turn 60, or the year you turn 61?

3. What year or age do you use the bend points from? I thought you use the bend points from the year you retire (2023 in my case), or do you use the published bend points for the year you turn 62? (I found some muddy legalese insinuating age 62 on the Social Security website).

Anyway, I’m appreciative of the effort you took to make this spreadsheet available, and I’m sure you know much more than I do on the questions I posed above.

Much Thanks

Congrats on collecting SS soon!

It’s true that I did not cap the earnings on the spreadsheet. The input in that column should be your SS wages (which are capped) and not your total earnings.

For the index factors, I take them directly from SSA.gov. They update them each year. I’m not sure how to answer the question about bend points. They’re based on how much you earned and when you earned it. Once you’ve passed them, you’re past them.

I don’t know if that helps, but I hope it does.

Best,

-PoF

Thank you for the direction! I finally reached someone at SSA who knew how their benefits are calculated. Not too many people there know more than the standard canned answers (and a robot could do that).

1. You set the index factor to 1 at your age 60. After digging through the SS webpages I found the page (that you mention in your reply) that gives the index factors; It requires you to enter your birthdate and calculates the index factor for you The results are the same as when you do the longhand math, like I did.

2. You use the bend point values from the year you turn 62.

After doing that, my own calculated benefits matched theirs exactly.

Low income earners will get up to 95% of their previous employment income each month from Social security. For higher earners: If you earned above $6,721 per month; you’re looking at getting 15% of that amount back in benefits, with a Social Security maximum of $3,627 – if you retire at full retirement age in 2023. Don’t count on luxurious living with that.

I’m glad you got to the bottom of this!

And I don’t think anyone who reads this blog is counting on living luxuriously on Social Security alone, although I have met some ex-pats in Mexico that are pretty much doing exactly that. Personally, I view SS as frosting on the top of a large cake of my own retirement savings.

Cheers!

-PoF

“And if you ever have 35 years of maximum contributions, there’s nothing you can do to increase your eventual benefit.” That assumes that one year’s max contribution, when indexed, is equal to every other year’s. In fact, the value for (max contribution) x (indexing factor) varies widely: looking at the last 35 years for someone my age, for example, that value has ranged from $130k to $148k, with the larger values being in the most recent years. So working another year, even if I’ve already topped out 35 times, could increase one of the earnings years by $18k, which would increase my AIME by $43, which would increase the monthly benefit at FRA by . . . $6. OK, not a huge amount, but it *is* possible to increase the benefit even if you already have 35 years of max contributions.

I stand corrected!

In medicine, we might refer to the extra $6 as statistically significant, but not clinically significant. Yes, the number is different, but it’s not going to make any material difference in your life.

Cheers!

-PoF

Great article. Quick question: you mentioned that the bend points are increased each year with inflation. Do those bend points STOP increasing once you hit a certain age, such as 60 or 62? I’d hate to think of my benefit going down once I’m in retirement because the bend points keep going up!

The bend points and index factors are updated every year, regardless of your age. Once you reach a bend point, it can’t be taken away from you — as the bend point bar is raised, so is the value of your prior contributions.

I hope that makes sense.

Cheers!

-PoF

That might be true for earnings before age 62, but the SSA site says that the indexing factor for age 62 and beyond will always be 1, regardless of inflation. In their words, “Earnings after [the year you turn 61], if any, are not indexed.” So if the years from 62 on are included in the top 35 (as they usually are), the AIME will not increase as much as the bend points. I turned 62 this year, so I guess I’ll know for sure in January how the bend points and AIME increase for me going forward.

Thank you for the detailed and impressive analysis and worksheet. You mentioned that expats may be out of luck if they have not contributed 40 quarters into SS. There actually are a few ways that they can. For many (but not all) developed countries there are Totalization Agreements with the US which will allow the time an expat contributes to the host country equivalent of SS to help meet the 40 quarters threshold. That doesn’t increase the amount received based on foreign earnings but can make one eligible when they otherwise would not be. When there isn’t a totalization agreement an expat is required to participate in US SS so they can potentially accumulate both the time credits and an increasing monetary benefit.

That’s good to know! It’s not an issue I will face, but others will benefit from that knowledge.

Cheers!

-PoF

I had already built a calculator like yours except mine didn’t need to look so pretty. I’m glad the numbers matched.

I’ve already retired at 56 and I plan to take my SS benefits at 62 (well-thought-out reasons).

My only question is whether I should apply in September or wait until January for the new AIME (due to inflation adjustment only) and the new bend points.

I already know that waiting another 4 months will increase my payout by 1.67%.

Four months probably won’t make any material difference in the grand scheme of things. If I had good, well-thought-out reasons to take it as soon as possible, I guess that’s what I’d probably do.

A few years ago, I decided I wasn’t up for working in my prior career (2 jobs that went south fast helped convince me), so I worked up what might happen with taking various retirment funds at different points in time. Taking most all of it when I was 62 vs 65 vs 67 vs 70, played out to have a crossover/breakeven point around 85. This includes several pensions from state employment that weren’t going up year-to-year (has to do with spousal survior benefits). The SS had an interest niche for us, where my spouse could get my spousal benefit and then switch to hers when she’s 70 (not longer available). My point is that it’s not a given that taking your retirement money early has a big negative effect on your finances. Setup the numerical analysis, helps to be good with spreadsheet calcs :-), and see how it plays out over time. You do need to look at having the money sooner and even what happens if you invest that money (even in CDs or similar). This is BEFORE you get into the whole having the money when you still have your health. For us, at 85, the breakeven point, it’s likely we aren’t going to have nearly as much fun as now.

That all makes sense, Dirk. I’ve seen quite a few analyses of the breakeven point, and it tends to be in the low-to-mid 80s, depending upon the assumptions. If you don’t expect to make it to 85, it can make sense to take it on time or early. And a younger spouse, especially if collecting based on half of the other spouse’s benefit, has a different calculation to do.

Also, if you can’t have fun without that Social Security money, by all means take it when you can. Most people running the numbers have other funds to use for fun; they’re just trying to maximize their lifelong benefit. Meanwhile, they’re also worried about what to do with large RMDs that they also don’t need to have fun. 🙂

Cheers!

-PoF

I came to learn about bend points, but I stayed for the humor…. I saw what you did there with finger joints and the 420 number line in the article…. Well done. Thanks for the article.

Thanks, bud. 😉

I look forward to this update every year. Looks like with my 2022 income I too will pass the 2nd bend point with a $6,490 AIME!

Does this change my savings/investing plan? Do I back off my earnings and savings rate? No. But it’s still cool to know.

Thanks!

Happy to hear it! It was fun to update this annually as I inched closer and closer to that all-important 2nd bend point.

It doesn’t necessarily change much of anything for me, either, but I will know that any additional money put towards Social Security, especially as a self-employed person paying both sides, is basically a terrible investment.

Cheers!

-PoF

Thanks for the updating the sheet!! I know I was gonna be close this year after updating your sheet for my info that year. Since I will be maxing out once again for 2022 it looks like I’m a whopping $9 beyond the second bend point now. 🙂

Pretty cool to see the progress from updating your spreadsheet the past couple years.

Thanks for the continued to work!

So, so close. You’ll rocket past it in 2023 unless you quit work for good before then.

Cheers!

-PoF

PoF,

I likely worded that terribly. I’m $9 BEYOND the 2nd bend point as my AIME is now $6181. 🙂

That said I plan to max out SS for atleast 2023 and 2024 so that should keep me solidly above that 2nd bend point going forward or atleast until the rules change. 😉

Nope — I read it too fast — my bad. You’re not behind, but beyond. Congrats!

I don’t quite understand your comment about a 30% penalty by taking SS early. You get less money over a longer time frame. By my calculation if you live to 82ish it’s the same overall total whether you take it at 62 or 71. Thus what you do with that money (ie reinvest to make even more) between 62 and 71 might make the difference. You could live a lot longer too, so I get it, its more complex to answer.

The annual pay is 30% less, but you’re obviously correct about collecting for a longer timeframe. The break-even point depends on the assumptions, but early 80s is about right.

The SSA’s actuarial tables give the average 62 y.o. man another 20 years to live; women get another 23 years. That’s an average, though, and it includes those with terminal illness and chronic, severe disease. If you are in relatively good health and do not have a family history of early demise, I still say the smart money’s on delaying to age 70.

If you’d like to hedge that bet, consider buying a SPIA.

Cheers!

Leif

Thank you – this is very helpful.

I’m looking forward to your updated calculator for 2022!

I update this every summer — look for it in June or July.

Cheers!

-PoF

Download had only xml and no worksheets. Didn’t work for me.

Should be a .xlsx file. Please download again and if it doesn’t work right, please let me know.

As an update, I have noticed that when downloading the Social Security calculator via PC it saves as a .ZIP file. Renaming the file extension from .ZIP to .XLSX allows it to open correctly in Excel and works fine. Thanks for all the work, working with it now!

I have no idea why some people get a .zip file. I’ve uploaded a .xlsx file and that’s what I get as a download when I enter my email in the subscription box.

But your workaround does indeed work. Thank you for pointing that out.

Best,

-PoF

I’ve managed to reach the 2nd bend point. I only plan to work 4 more years so will have 4 low years and likely 5 years of not quite max with 20 years of paying the maximum. I’ll take it.

Great post. One of the things that I had no idea when I first learned about social security was, well if I earned 40 credits am I good for the rest of my life? No point in working anymore? Not so fast.

As you’ve highlighted, it’s the best 35 lucrative years. Zeros fill in the rest. Using my current contributions to social security, I was amazed at the results at what my estimated benefit will be. However, I think the benefit is supposed to decline if I don’t continue to earn as much going forward.

I was very sad that day.

I am a huge fan of this blog and I appreciate the above analysis on social security timing of collection. However, your analysis is predicated on living a really long time and may perhaps be flawed. You should also include the “break even” analysis collection at 62, 65, and 70. Now at age 57 and well beyond the second bend point, I am planning on collecting at 62 as my break even age is 79-80 yrs old. I look upon this money as “collecting when I can” in addition to protecting tax deferred and Roth funds thereby allowing that yearly sum to further compound.

Appreciate your pro/con on the above

Is the first bend point for 2021 966 or did you mean 996? Thank you.

Yeah, it looks like you’re right. I see the same thing and double checked in the SSA website and it should be $996. Makes a difference in the calculations for sure.

Dang — you’re right. I’ll make the appropriate edits. The numbers will change a bit, but not in a “clinically significant” way.

Leif, I attempted to download the latest version of the spreadsheet, but the zip file only contained XML files and no .xlsx files. Something with the zip, or something with me?

Thanks again for putting it together.

Really appreciate your SS Bend point calculator. Thank you. Hubs (61) will retire end of first quarter this year (2021), so that he can better manage the symptoms of Parkinson’s by pacing himself, reducing stress and exercising more. He is an insurance agency owner with an excellent own occupation disability policy we purchased 30+ years ago. My project as I get ready to set up the new year’s office payroll was to figure out if he should take W-2 wages going forward or not. The benefit to his eventual SS payout would be replacing a year where his index income was 62261. (So he would need to earn wages and pay social security tax on more than $62261 before he retires to improve his benefit AT ALL). At $62261, that requires employer and employee FICA contributions of $7220.36 plus medicare taxes. (Half of that from our “paycheck”, half as a business expense, since he is also the business owner.). That extra $7220 would be taxable to us, of course, but it looks like we will have some S Corp income discounted from rule 199A, and will be in a lower tax bracket due to the tax free replaced income from the disability policy.

Looks like I will simplify our bookkeeping and increase our income this year by forgoing his paycheck, and make it up in owners distributions and quarterly tax payments. Thanks again for your efforts and generosity in building and sharing the spreadsheet.

I’m glad the post helped you navigate a complex situation, and I’m sorry to hear of your husband’s diagnosis. Parkinson’s can be a rough one, but if the symptoms can be managed, he’ll have a better life. Eliminating the stress of work is one way to ease that burden.

Best,

-PoF

Dear Good People,

The Social Security Bend Points….These are not as simple as they look (it’s like figuring out the delta/delta equation in ABGs, you can do it but it takes some effort time). I thought the above was a good introduction, but after a deep dive into my own finances I found some other resources fellow providers may find useful.

In fact on this COVID Saturday, I spent over an hour figuring out my Social Security estimate based on (forecasted) Bend Points.

The best resource for this I found was at the link below from Social Security Intelligence

https://www.youtube.com/watch?v=im1IYEa_B2o

Again, it takes time. It’s best to Google My Social Security.gov and then go to that website and find a history of all your reported earnings. Create a spreadsheet with 5 columns (Year, Age at that specified year, Earnings, Indexed Factor and then Indexed Earnings) You then have to write down every single reported annual earning. You then have to find the Index Factor which is given to you in the above video (or you can Google it). You then have to multiply every single year by the Index Factor in order to get every year’s Indexed Earning.

You then take the entire Indexed Earnings and divide the total number by 420 (the number of months in 35 years, upon which your Social Security is determined). Once you do that you have your Average Indexed Monthly Income (or AIME)

Congratulations! You’ve completed the first step

Once you have your AIME, you must then find your Bend Points. As most reading this are not yet 62, you will have to estimate the Bend Points for when you are 62. Again, the video above gives information on how to do this. For instance, the current Bend Points for 2020 are 960 and 5785. If you were born in 1975 and assume a 2% annual increase in salaries, then the Bend Points for when you are 62 would be estimated at approximately $1344 and $8100. You then need to calculate your Primary Insurance Amount or PIA based on calculations of these Bend Points.

I like your calculator but why doesn’t it match the current calculations from the IRS’s site?

I’ve always found social security to be complicated to fully understand

This is one of the best articles I’ve read on it

Thank you for sharing

Can you please provide some clarity on the options non-US citizens have to claim their social security once they have accumulated the required minimum 40 credits? I have Indian citizenship and even though I have tried reading through the documents available on SSA’s website, it hasn’t been clear if non-US citizens can claim SS once they have moved back to India, during their retirement.

It doesn’t sound like that’s an option unless you continue to live in the U.S. at least part-time.

“Non-Citizens Who Leave the United States

When some non-citizens leave the United States for six months or more, their benefits stop. To resume receiving benefits, they must return to the United States for at least a month. There may be additional rules pertaining to those receiving Social Security benefits as a surviving spouse or a dependent.”

https://www.investopedia.com/articles/retirement/072016/how-advise-nonus-citizens-social-security.asp

Best,

-PoF

Thanks. I have been trying to research on this topic and wanted to make sure i am not missing anything. I found the following verbiage here on SSA’s website under point 5(a) of this guide – https://www.ssa.gov/pubs/EN-05-10137.pdf

5. If you are a citizen of one of the countries listed in the chart below, we will continue to pay your benefits outside the United States if:

a) You are receiving benefits based on your own earnings, and you earned at least 40 credits under the U.S. Social Security system or lived at least 10 years in the United States; or

b) You are receiving benefits as a dependent or survivor of a worker who earned at least 40 credits under the U.S. Social Security system or lived in the United States

for at least 10 years. You must also meet the conditions under the heading “Additional residency requirements for dependents and survivors” in this publication.

• Afghanistan

• Bangladesh

• Bhutan

• Botswana

• Burma

• Burundi

• Cameroon

• Cabo Verde

• Central African Republic

• Chad

• China

• Congo, Rep. of

• Eritrea

• Ethiopia

• Fiji

• Gambia

• Ghana

• Haiti

• Honduras

• India

• Indonesia

• Kenya

• Laos

• Lebanon

• Lesotho

• Liberia

• Madagascar

• Malawi

• Malaysia

• Mali

• Mauritania

• Mauritius

• Morocco

• Nepal

• Nigeria

• Pakistan

• Senegal

• Sierra Leone

• Singapore

• Solomon Islands

• Somalia

• South Africa

• Sri Lanka

• Sudan

• Swaziland

• Taiwan

• Tanzania

• Thailand

• Togo

• Tonga

• Tunisia

• Uganda

• Yemen

Based on this, I would imagine Indian citizens would be eligible to receive their SS payments once they leave US and move back to India?

This statement appears to be key: “You must also meet the conditions under the heading “Additional residency requirements for dependents and survivors” in this publication.”

I would call or visit your local Social Security office and they should be able to clarify. https://www.ssa.gov/locator/

Best,

-PoF

FYI, your updated numbers for bend points are not consistent throughout the article. Numbers provided in summary box graphic do not match the numbers listed in the text in subsequent paragraphs.

Spouse and I both nearly the same age, and both past the second bend point. Our AIME’s are both north of $7000. Will we each receive our full benefit, or is there some sort of “family maximum” to be aware of? If we exceed the family maximum, that might be a reason to claim earlier than 70.

I can’t find any easily interpretable info on this. Can anyone clarify?

One thing to consider when bending is what SS does for you. PoF says half his retirement income post age 70 will be SS. If you’ve been planning a 4% retirement that lowers your WR to 2% on the portfolio. Pretty much bullet proof to failure. Since I’m a big fan of epoch retirement where one epoch meets another you can break up your retirement spending. Early retirement could be WR = 5 or 6% if your old age spending is going to be 2% it changes the calculus. It’s worth thinking about that when deciding on when to retire. In my case I pulled de-risked a big amount (several hundred K) to Roth convert so I am doing this exact thing pulling a lot now for a later payoff in tax savings starting at age 70. The market is up massively so this is the right time for me to do this, sell high as they say so I did. Blowing off 15% is blowing off a larger percentage of SORR protection in old age and I consider age 70 SS as a premier SORR hedge. 15% less SS means 15% more has to come out of the portfolio and a greater vulnerability to SORR just at the time you won’t be able to cop a side gig. It’s easy throw away money when your making a lot in W2 land, less easy when that money is actually at risk. Just food for thought There is no reason not to tier your retirement income according to epoch beside some using some fixed constant and there are many variable withdrawal schemes out there. But a longer high withdrawal rate early (say between FIRE and age 70) could mean a worse picture once SS kicks in, a shorter high withdrawal period could work out just dandy.

I used the previous PoF spreadsheet for SS bend points and found it did a good job of estimating my benefits if I stopped working now.

I did have to update the inflation multipliers since I was born before 1960 but that was a minor task.

The nice thing about this spreadsheet is that it shows just how little change one gets by continuing to work past the 2nd bend point, especially when you already have 35 years of work history and in spite of my early work years showing very low income.

Lynne – If you don’t yet have 35 years of work history, would you say its recommended to at a minimum get a little bit of W-2 income once you are FIRE just to reach the 2nd bend point, thus eliminating a few zeros from your calculation?

I don’t see where it would hurt to get some income and it certainly would help to erase some zero years, which could substantially impact your benefit amount. Maxing out income in your recent earning years also makes a big difference. You are quite young, so likely you don’t have more than maybe 10-20 work history years now. It doesn’t have to be W-2 income either; self employment counts as well (you just get stuck contributing the other half of SS/Medicare).

If you want to prove to yourself the value, play around with the PoF spreadsheet and start out with only your current work years to see what your AIME is now. The SS website also has a “can I retire early” calculator where you can put in your actual income for each year and I “think” I recall it has ability for you to put in expected income in future years. If not, go back to the PoF spreadsheet and enter maybe $4,000-5,000 in some of those zero earning years, to see the effect it has on your overall picture. I chose the lower $ amount to counteract the effect of the inflation multiplier on older earnings years. If you want to get really precise then take your future earnings $ and reverse calculate using the inflation multiplier to get back to what today’s dollar was worth some years ago.

I made sure I got my 35 years’ work history and won’t file for SS until age 70, unless I get some bad medical news down the road. Both my parents are in their mid/upper 80s despite bad health habits, and my grandparents lived well into their 80s, so longevity is in my family.

Interestingly, both my parents filed for SS at age 62 and both seemed to regret that decision later in life because the COLAs do not keep up with real world inflation. And I see that most or all of COLAs today are eaten up with higher payments for Medicare.

There is serious political risk of means testing to get SS benefits going forward. No one is going to feel sorry for well off retires with fat 401k’s. If you think the government wouldn’t punish people who relied on current policy to make plans think again: Obama raised taxes retroactively but kindly provided 5 years for me to pay the extra 30k.

Take the money as soon as you can is what I’m going to do at 62.

This was one of my favorite posts you did Leif and first opened my eyes to these bend points on social security when I first read it. Thanks for the update and improved spreadsheet which I plan on using.

I too think Social Security will be there for us but it will be drastically different in benefits compared to current users. More likely workers are going to have to contribute more to the system to support the retirees and easiest way to do that is to raise the income cap which gets taxed (I have previously written about how this is like a massive forced Ponzi scheme).

BendPoints is back! PoF, this is a classic and sets you apart from all the rest! I remember thinking about this a while back and looking around for quality information. It is all here in this post!

Great article – What if you haven’t reached the 2nd bend point on your overall record? Couldn’t you just continue to earn $5,397 each year while being retired before collecting SS to satisfy that? Seems like an easy way to erase some zeros from that 30 something year average they use to calculate your PIA.

I’ve been in Max SS territory for about 5 years, but I’m only 35 so lots of “high school and just out of college” earning years factored in right now.

I’m certainly not making this a primary part of my retirement, but why not play the game well now to maximize the benefit later.

It depends on what you mean by “earn” as a lot of income streams in retirement will not result in SS contributions. But if you’re replacing zeroes or very low income years with higher earning years, your eventual benefit will increase.

Best,

-PoF

Agree – Earnings would have to be qualified here. To keep it simple lets say its a part time job of some sort that results in some W-2 earnings. In theory a few years of at least $5,397 would help replace some zeros. Trying to get any incremental earnings past the 2nd bend point is essentially low yield when it comes to maximizing SS benefits especially considering the go to not work a w-2 job because I need to.

I’m certainly not saying that working to $5,397 is the way to go long term, but as someone who is young (and on the path to FIRE around age 40) trying to erase or avoid a few zeros while I get myself from 40 to 60 something it seems like the prudent thing to do.

Any holes in my my assumption?

This is all quite interesting. I find it difficult to calculate what I will receive because I was a teacher for 15 years. Although I’ve been paying into SS, I will be subject to a Windfall Elimination Provision (WEP), which I hear could lessen what I receive by up to 45%. I rarely see this subject mentioned in financial planning. (This is also a warning for those considering teaching as a second career).

Regarding your statement “It’s a no-brainer if the spouse’s benefit based on his or her own record will be lower than the spousal benefit. Collect own benefit from age 62 to 67, then switch to the higher spousal benefit.” Have you considered the 2015 changes that made some “double dipping” benefits unavailable to those of us born January 1954 and thereafter? See website https://www.thebalance.com/social-security-strategy-for-marrieds-age-62-2388923

I will have to dig deeper into this – thank you for the link. I loaned Mike Piper’s book on the topic to my father, but will ask for it back tonight!

In the meantime, I’ll edit the text as it appears what I described may not be an option for my generation.

Best,

-PoF

I was asked a question about what income level would be a good one to report-if that is in your control- so that you get the 90% and 32% bend points but not the measly 15% bend point factor. I THINK the correct answer is $48,642-the Average Wage Index-that is reportd at SS. Client is 51 and is currently reporting less than that but could probably adjust that higher. When populating the 35 years my assumption is that each year “bends” at the current year’s AWI. Any thoughts on that?

My initial thought is that the current tax implications of how much money to take as salary versus distribution (I’m assuming this is an S-corp setup) are much more impactful than the eventual SS implications of that decision.

With the TCJA and the 20% QBI deduction per Section 199A, the decision becomes more complicated, but S-Corps have become much less advantageous.

Best,

-PoF

Thanks for the great calculator. As I use it, I wonder what are the meaning of the “Index Factor” and “Index Wages”. Do they apply at all to the discussion here or are they used for another topic? Thanks again for all your hard work on this!

Thanks POF for the clear explanation and calculator. As I wind down my part-time position to fully FIRE I always wondered how to estimate SS and frankly, like most, just ignored it in my calculations for retirement planning. I was happy to see that I was past the second bend point and agree with you SS should be around in some form for me by age 70. Also your calculator finally spurred me to register on the SSA gov site (long overdue).

Cool. Interesting what it takes to get us to overcome the inertia of standing still.

Congrats on reaching the second bend point — and my condolences for the fact that your contributions now mean very little.

Cheers!

-PoF

Perfect timing, earlier this month I maxed out my SS tax for 2018 ($7960.80). In your calculator I typed in $128,400 for 2018 and apparently I just hit the second bend point this month! AIME of $5398 vs $5397.

Kind of discouraging to know that I will not receive 85% of my future SS withholdings.

Thank you so much for the calculator and the clear explanation! So very helpful and very much appreciated. I read about bend points for the first time right before we ERd at 53 a few years ago and noted that DH and I were both past the 2nd bend point, but this is the first really clear calculator I have seen that will be so helpful to so many. It really helps to illustrate that working way past the 2nd bend point should not be for SS purposes. To sock more $ away, maybe, but not for SS! Thank you so much!

Thank you for sharing, and congrats on being past that second bend point! I’m a few years shy, but if I keep this website going into 2022, we should get there.

I’m pretty sure my wife will be collecting half of my benefit unless something changes that we don’t anticipate.

Cheers!

-PoF

The last time I checked, I was pretty close to the second bend point. More work at this point isn’t going to increase my benefit much.

My father in law uses his social security benefit as a donation fund. I think that’s a great idea and will aim for the same. Hopefully, we won’t need it.

There is some value to getting to that second bend point, and as long as you’re making some income from the blog, you’re inching ever closer. After you hit that mark, the additional benefit of further contributions is less than half what it was before.

Cheers!

-PoF

Great article! I did not realize the way bend points work. Very insightful eapecially if you are a small business owner and you hit the 2nd bend. You should strategize on how you pay yourself (payroll vs draw).

I dont understand why so many people are against taking SS at 62. It would take me 10 years from the age of 67 to actually hit the break even point where the sum(earnings from 67-77) becomes > than the sum (earnings 62-77). It wouldnt be until i am 77 that it becomes worth it and by then theres no guarantee Im even alive. Im a big fan of FIRE because I value my personal time and want to do more when Im younger. What is the extra $ is going to get me when im > 77 ? Many people cant do the same things when they were younger and have to cut down lots of activities due to medical limitations. Just my 2 cents :-).

BTW – I noticed cell C130 may be hard coded to your amount and not a sum of the indexed values. You may want to correct that. Hope this helps.

Thanks for the tip on the hard coding. I’m away from home and using Excel Online to make edits — unfortunately, it’s not as robust as the full program and a number of formulas were left out and only the values transferred over.

I’ve corrected the sheet now, and the new sheets are available via the download buttons in the article.

The debate about when to take SS is an ongoing one. The break-even point for waiting is somewhere in the early to late eighties, depending on the assumptions of returns on the money. Of course, if you need the money to fund your lifestyle at 62, there’s no debate. WCI and Dr. Cory S. Fawcett did a pro/con on this subject.

Cheers!

-PoF

Interesting link! I can definitely see this debate has so many different financial angles coupled with life events one can not predict.

Glad I was able to help on the excel.

I also don’t understand the debate.

If you know exactly when you’re going to die, the decision is easy. Otherwise, you place your bets and you take your chances, eh?

Still, as POF said – if you need the money at 62 then you gotta take it (and maybe change your lifestyle a bit); else it’s probably safer to hold off from a risk mitigation standpoint, not necessarily from a wealth building standpoint.

Thanks for the awesome update! It brings home a point that a lot of physicians don’t know: early retirees will have a lot of zeros averaged in. It is a factor to consider. Maybe working longer or part-time work wouldn’t be so bad (sorry for the heretical remarks on a Fire website!)

Only you could make a social security calculation of 12 x 35 funny and interesting!

Just wanted to thank you for the calculator. I was about to make one and figured I would do a search. Behold my long time online acquaintance created one for me.

Thanks,

One of the key elements in any discussion regarding when to claim Social Security benefits seems to be the breakeven point: The age at which you receive more cumulative benefits by delaying your claim.

The problem with using the breakeven point to make your decision on when to claim benefits is that it is unknown until you file a claim for Social Security. Two factors that make calculating your breakeven point difficult are continued employment which changes your PIA and COLA that you are deemed to have earned from age 62.

For example, I continued working until age 68. This removed 6 of my lowest earning years from my PIA calculation. I received raises between ages 62 and 68 increasing my PIA from what Social Security had projected. COLA for the 6 years that I had delayed my claim was applied to the PIA. My monthly Social Security benefit came to within $150 of the PIA that Social Security projected I would receive at 70.

After discovering that COLA was the reason that my monthly benefit was more than I had expected, I decided out of curiosity to calculate my breakeven point based on the PIA I could have received at 62. It came out to be between the ages of 76 and 77 based on actual COLA and wasn’t affected by what I used for future COLA.

My conclusion is that your breakeven point isn’t a very good metric for deciding when to claim Social Security benefits unless you quite working at age 62 or earlier. You’re better off making the decision based on whether or not the benefit covers your basic living expenses.

Thank you for your thoughts, Panda.

This is a site for aspiring early retirees, but you do make a good point about taking SS early versus padding the earnings record in your sixties. You definitely don’t want to take SS early if you are working. Prior to full retirement age (66 to 67 depending on date of birth), your benefit is reduced $1 for every $2 you earn above the 2018 limit of $17,040. [reference]

Best,

-PoF

I am 62 and have been retired for 4 years. I work a little bit on the side. I am past the 2nd bend and waiting to draw SS. I could make a ton of money between now and then but it will barely increase my monthly payment. The biggest impact on my payment is to just delay as long as I can.

I agree completely. The ROI on your Social Security tax past the second bend point is terrible, but there’s not much you can do about it. If you’re in good health in your sixties, delaying to 70 makes a lot of sense.

Cheers!

-PoF

Good discussion PoF. Calculating the “crossover” point to decide whether to claim benefits at 62 or 70 (or whenever) is not necessarily a simple spreadsheet. If you are close to claiming and have a spouse who also qualifies based on their earnings, it can get a bit complex regarding what is the best way to claim benefits to maximize the return.

The “how will we get the most $$” calculation may not be very accurate if you don’t include tax effects and the effect of RMD income from your IRAs once you turn 70. SS income is taxed at different rates depending upon your total income.

For our situation, it turns out we get more after tax income by drawing down the IRAs to live on for a few years and waiting until 70 to claim SS benefits. Depending upon your drawdown needs and the amount in your IRAs, it could result in much lower RMDs at 70 and then the SS income does not kick you into a higher tax bracket.

Investigating what you end up with after taxes is what matters to help decide when it is best to start SS benefits.

That makes sense to me. It’s absolutely an individual decision, and you should also factor in you and your partner’s health.

If you’re both healthier than the average person your age, you’ve got a good chance of outliving the actuarial tables, and delaying makes more sense. If you’ve got a heart full of stents, type II diabetes, and oxygen dependent COPD, you should start collecting yesterday!

Best,

-PoF

I’ve run calculators and run calculators on this.

Unless you are rather sure you are going to earn 0% on your investments for a time frame of over a decade, you are financially best off to take the money at 62.

You do not get nominally more money until age 82 if you wait until 70, and that assumes the money earned 0%.

If it earns even 3-4%, that stretches your age up to late 80s, even 90s before you have more money from social security.

I don’t know about you, but my travel(and almost surely overall) expenses will be much lower at 85 than 65

There are other advantages to postponing till 70. I’m Roth converting while living on cash. Since I live on cash my tax bill is zero so I can convert to the upper limit of the present 15% bracket which is 75,900 per year AGI. Since the standard deduction is 12000 that’s 87,900 I can Roth convert at a 15% rate. If I was taking SS it would dramatically reduce my conversion at the 15% level. Also I have a younger wife who is a SAHM and running my SS up to age 70 improves her take to 21K instead of 15K when I kick the bucket. Trump’s tax proposal improves this by allowing me to Roth convert about 114K per year at a 12% tax rate if they ever pass the damn thing. This is a boon to those of us that maxed out pre-retirement accounts over 20+ years by allowing us to unload at a low rate.

4 advantages:

1. my SS grows 8% per year inflation adjusted

2. by cleaning a lot out of my tIRA, my RMD plus SS at 70 will be below 114K per year, (hopefully just below). My Roth will remain untouched and aggressively invested in an efficient frontier portfolio which has a better risk adjusted return compared to a Bogel portfolio . I will supplement my needs (new car, trip to Asia or something) by selling post tax stock mixed with LT cap loss. A higher SS+RMD yet under 15% (or 12%) means I have to take less out of the post tax account which improves its longevity. The Roth remains a transfer of wealth vehicle unless it hits the fan.

3. My SS is inflation protected. When my wife files at FRA we will both have a maxed out inflation protected annuity happening.

4 My wife will make a little more when I become absent.

So there are other pretty dramatic advantages to taking at 70 not considered by calculators.

I was messing with Big ERN’s retirement google sheet.

https://earlyretirementnow.com/2017/01/25/the-ultimate-guide-to-safe-withdrawal-rates-part-7-toolbox/

Adding just my SS at age 70 (not including my wife) increased my 100% safe withdrawal rate 0.9% from 3% to 3.9% THAT’S A LOT OF DOUGH. Personally I don’t believe in the 4% 25x rule, but I do believe in Big ERN’s method of calculation. I think SS will definitely “be there” even with the 25% haircut. (If you get to 132% and take a 25% haircut you will be at 99% of your FRA! and your survivor will also benefit. You can adjust this haircut into Big ERN’s sheet as well and get a good idea of how it will affect your SWR.

I’m older than you whipper snappers, In 4 months I will reach the 3rd knuckle, FRA but my rate of Return will be 8% per year so I’ll have to go back to the Capitate Metacarpal joint to get the full picture.

Your wife’s benefit is 50% of your bene at your FRA (if she takes it at her FRA). Her payout will not increase even if you wait until you are 70 yo.

I only know this because I bought Maximize My Social Security (Laurence Kotlikoff’s product) and reviewed it with that service. My wife is 11 years younger.

The problem I see is with the bend points changing with inflation. This probably would not affect someone close to receiving SS benefits, but certainly it would affect the retire early crowd.

As an example, I will hit the FRA in 29 years. At that time (using the CPI Inflation calculator in reverse), the first bend point would be 1872 and the second bend point would be 3785. This translates out into total SS contributions of 786,240 to hit the first bend point and 4,740,540 to hit the second bend point. Unless the yearly SS contributions change significantly, it seems unlikely to hit the second bend point.

Or is my math and assumptions incorrect?

I’m not sure I follow the math, Seth, but I’m guessing you went south somewhere.

The bend points will continue to grow, but so will the value of your past contributions as the index factor for prior years increases. They should grow at the same rate. Here’s a list of the bend points by year going back to 1979.

Best,

-PoF

OK, I see. I forgot about the index factor. Definitely more complicated calculation. Thanks

PoF,

Have you considered the advantage of claiming at 62 (with the 30% reduction of benefits) but investing the funds rather than consuming them? Actuarially speaking, the benefit value should be equivalent (over your lifespan) but you protect yourself against an accidental/premature death risk. That is, if you are in great health and expect to live to 100 and delay benefits until age 70…but, you get hit by a car at age 69, you (and you heirs) missed out on 7 years of SS benefits that is not replaced. Seems like an unnecessary risk of leaving as much as $105,000 on the table. Am I wrong?

Dan

It’s designed to be more or less a tossup. Taking it early is a bet against yourself (as is insurance). Based on genetics and reasonably healthy living, I’m guessing I’ll outlive the actuarial table and if I’m right, postponing will win.

According to this article from Time, 80.5 is the break-even point.

Cheers!

-PoF

Thanks for the reply…and sure, 80.5 is the break-even if you exclude the ability to invest the benefits rather than consuming them. Investing the benefits pushes the break-even point out much further but, of course, is contingent upon returns.

I will ABSOLUTELY, no questions asked, take my benefits early for the simple reason that I don’t need them. Since my lower benefits earned for a longer period will be invested for more years than your higher benefits earned for a shorter period, we will probably come out at the EXACT SAME PLACE…(we both win!!!). But in the off chance that I die earlier than expected, I won’t miss out on collecting any benefits (a small, but real risk…but not a “bet against yourself”).

Sorry to quibble, but I just wanted to add an additional thought to the mix.

Greatly appreciate your work,

Dan

Dan’s point is exactly how I’ve been thinking about this as well. If, as an early retiree with sufficient assets to not need SS, doesn’t it make more sense to take the earliest distribution? I put together a spreadsheet really quickly to try the math on investing the benefits at 8% annual growth given different benefit amounts and start dates (62, 67, 70). Benefits are based on my current SS benefits (yay, past the second bend point!). Please poke holes in my math … but seems like you come ahead by $4.4 M in total lifetime benefits starting at 62 instead of 70 living to 85. Here’s a link to the spreadsheet: !ApMK-Fx03mqcwuAp9iFaSyBNv0k04A

Mike

Your assumption though is that you can invest at 8%. No one can predict what market returns will be over that 8 year time span, whereas delaying is giving you a guaranteed 8% return. While I understand your logic and you do accumulate 8 more years of benefit, you are risking a long term benefit reduction if you live a long life.

I think as you get older the numbers ss sends you are more accurate. I will put my numbers in on my 4 day weekend. I am pretty sure I am beyond the second bend. I also have finally eliminated all the zero years when I did not have job in med school.

This post didn’t quite bend me out of shape, POF, so thanks for doing this. ? With significant part of my earnings history outside US, I knew I wouldn’t reach the second bend point. My SS earnings record has pegged me at $15K benefit per year when I turn 67, but I have considered only $10K/yr SS in my financial plan considering we may receive only 75% of benefit amount if Congress does nothing. Still, this is a decent sum and reduces my portfolio WR so am happy to get it, but I am not quite looking forward to turning 67 though yet ?

The last time I looked, I was pretty close to the second bend point, but not quite there yet. With my current income, I don’t think there would be much progress from 2 years ago.

Nice spreadsheet, though. I will input my numbers today.

Yeap, I look at it as icing on the cake too. Unless I die early, then the benefit will be very helpful for my family.

How do you know how close you are to the second bend point?

Nice write up PoF. I looked into this a couple of years ago and realized I was pretty close to the second bend point. For the vast majority of docs, they will be well past the second bend point by the end of their career. It’s important to get enough credits, and working up to at least the first bend point is high return on investment.

I love this calculator and the explanation. We’re still over 30 years from standard retirement age, so we’re assuming it won’t be there. Realistically, I think something will be there, but I would rather save too much earlier when I have more compounding time working for us. We have plenty of time to reevaluate how much social security will be available as we get older. Worst case, we are fine. Best case, we can retire earlier or with more wealth.

Most of us look at it as icing on the cake.

The fact is, for an early retiree, the amount of money you’ll have in your sixties and seventies depends much more on total return and sequence of returns, but it’s comforting to know that some significant money should be there some day.

Cheers!

-PoF

Thanks for breaking this down. I’ve never focused a whole lot on SS, which you point out is a fairly typical thing for people like us (FI/FIRE). But I agree that we’ll have something in some form, whether it’s SS or UBI (universal basic income). A lot of younger folks think that SS will be history in 40 years’ time. But again, I think we’ll have something. It would be ridiculous not to. Given that most people won’t have much saved up for retirement (personally saved up). I’ve also never thought about “bend points.” I knew there were diminishing returns at some point, but never did the research. Again because I don’t really think much about SS.

Thanks, TK.

I was somewhat familiar with the Bend Point concept, but had never done the math for myself. I had been putting off writing this one, because I knew it needed a calculator, and that would require a big effort, but it was well worth the time.

Cheers!

-PoF

Nice post on a topic that isn’t covered much for early retirees. What is nice is that so much of the benefit occurs early in your working career, especially if you have a high-income. So even if you retire early, you’ll still get a good portion of your SS benefits (in whatever form they exist at the time).

I have enough “golden handcuffs” angst with my job. I’m glad SS is so progressive that there is little benefit to working much beyond 10-15 years.

I simply forget it in my plans (like many seem to do) and consider it free financial longevity insurance in my old age in case I need it.

Thanks, SIBF.

I don’t necessarily forget it, but I don’t think about it much. I don’t anticipate taking a penny from it in the first 25 years of FIRE, so it feels pretty abstract.

I know it’s theoretically possible and even probable, like the Vikings winning a Super Bowl someday, but I’ll believe it when I see it.

Cheers!

-PoF

Even early-retired I’m passed the second bend point. Additional working years wouldn’t add very much at all to my benefits. But I’m also not banking on it. If it’s still available when I hit 70, then I’ll take it and start partying. 🙂

That’s a good place to be, FCB.

Like you, assuming some benefit exists (and I believe it will), I’m gonna party like it’s 2045!

Cheers!

-PoF

Good stuff PoF! I just wanted to point out that this isn’t completely accurate: “If you failed to earn income for 10 years (40 three-month quarters of at least an inflation-adjusted $1,300 income), you’re not eligible.” You do need to earn 40 credits, but it doesn’t have to take a full 10 years to do so. The smallest amount of time you can earn your credits is 8 years and 2 months – you are limited to 4 credits a year, but you can earn all 4 credits in a single month. Source: me. I qualified for SS in 8 years and 4 months (I haven’t even been in this country for a decade yet!).

You’re right — the US government has some wacky definitions. A three-month quarter is the equivalent of earning about $1,300. If you earn $5,200 in a day, you’ve got a year’s worth of SS earnings knocked out.

Technically, you could qualify with only 10 days of earnings, as long as they are lucrative days in 10 different calendar years.

Cheers!

-PoF

It’s a shame that something intended to help the poor and be a safety net is so dang complicated!

Thanks for your spreadsheet. It definitely adds another layer of thought to our RE date.

For most of us, Social Security is the closest thing to a pension we’ll see. Might as well try to get the most of it if you find yourself shy of the 2nd bend point.

After that, the additional benefit from increasing AIME is less than half what it was prior to the 2nd bend.

Cheers!

-PoF

Interesting. I conceptually got the cutoffs and that bend points existed but I’ve never seen the actual points as written. While unlike some I do believe social security will exist when I retire. I expect benefits will change before I retire, potentially changing the bend points.

Same here. Having researched it for the article, I have a much better understanding now, as well.

Cheers!

-PoF

Nice post. I had not given this much thought but recently my mother was debating whether to take SS early (she is 62). She deferred for now.

The more I read the more I lean towards her taking funds early. My dad has earned more in his life and is 12 years older then her. Chances are he will pass before she does and in that case she will get his full SS payments. So now I am leaning towards her taking the SS payments at age 63. Thoughts?

That’s a tricky one. Full retirement age for her would be 66 (or 66 & 2 months) and he’ll be 78 then. If he is in relatively poor health, it would make sense for her to take benefits sooner than later.

If he’s healthy for his age, this might be a job for a spreadsheet. Good luck!

Best,

-PoF

It sounds like she’d be best off taking SS now if he has already taken his, and his benefit now is far larger than hers would be if she waited until age 70 and took half his SS amount in the meantime.

Very cool PoF. Will download the tool to see how the numbers for Mr and Mrs PIE compare to the summary projections spat out at us over at ssa.gov.

Here’s to a healthy retirement and none of those interphalangeal joints becoming arthritic and bending permanently too far. Those pro-inflammatory cytokines (TNFalpha, IL-6 and IL-1) will get your joints and your SS projections. Bet you didn’t expect to see that type of comment in a SS post! Your readers will be scared away by this sort of stuff from me…. :>)

You joke about tumor necrosis factor and interleukins, but many people I know who retire in their fifties and sixties are sadly quite limited by arthritis.

I still want to be able to run, climb, bike, ski, etc… and do it all as a retiree long before I collect Social Security.

Cheers!

-PoF

Indeed. Spending the last 20 years working on therapeutics to alleviate diseases such as RA, PsA and OA, I know the challenges and unmet medical need all to well. When I pull the plug, will be able to speak more about what my company and my teams specifically contributed to that endeavor. It is brutally hard yet great strides have taken place, which is the rewarding part of our teamwork with research scientists, clinicians and most importantly the patients.

Great article! I really like the calculators.

I did notice a couple of typos in the Social Security tab of the calculator spreadsheet:

Cell E75 is: =IF(E69>5536,E69-5536,0)

Cell E75 should be: =IF(E69>5336,E69-5336,0)

Cell G80 should be: 80%

Thanks! Let me take a look. Excel is hard.

Oh, turns out I’ve got things correct in the single file used to embed the spreadsheet on the calculator page, but not in the downloadable. That will be fixed momentarily.

Thanks!

-PoF

Uh oh! Does that mean I miscalculated and have to work another 17 years? :O

Yes. Yes, it does. ?

Thank you for the post and Excel spreadsheet. Extrapolating the benefit of future contributions prior to possible early retirement shows that for each additional year of work I would only add about $439 to the annual social security payments. Adding $10,975 to my retirement nest egg would generate the same income at a 4% SWR.

Working adds to the nest egg and adds to social security benefit so it is not an either-or choice. But, as you pointed out, working just for social security benefit is a poor investment.

That’s a great comparison to make. The increase in Social Security is a pittance compared to what a physician can sock away by working one more year.

Cheers!

-PoF

My AIME is $6965, well past the second bend on the curve, with 35 plus years of earning. Any additional work years as a doc will replace very low earnings years of adolescence but probably will not move the needle all that much toward actual retirement benefit.

This has been a very useful tool for me. Thank you for doing it. I previously estimated the benefit, with a number somewhat pulled from air, somewhat calculated from the ssa.gov site, but now I have a better idea what the actual number will be. (My guess was pretty close!)

The VagabondMD AIMEs high!

You’re in great shape, obviously. I’d like to cross over to beyond the second bend point, but I’m not going to alter my life’s plans to do so.

Cheers!

-PoF

I just assumed SS wouldn’t be there when I could take advantage of it so never dedicated any time to learning about it. This is good to know at least. Thanks PoF!

The good news is that the shortfall is easy to fix. Did you notice the amount you’re taxed on jump from $118,500 to $127,200 in one year?

A few more $8,700 jumps and the funding issue is solved.

Another problem is the increasing roles of people making the move from welfare to SS disability. There are actually companies contracted to get people converted and are rewarded monetarily by state governments for each person they get off of welfare and into disability. I heard it on NPR a few years ago and was thoroughly disgusted. Of course, some physicians are complicit in this scheme.

Best,

-PoF

Oh good grief on the transition from welfare to disability! It appalls me that society has gotten so much more comfortable with sloth.

I entered my numbers on your spreadsheet from the hard copy SSA document that I got in the mail last fall. When you near the big “5-0” this is one of the “gifts” you get (in addition to many copies of your AARP card!) I’ve reached the first bend point too, but since I’m leaving full-time work this Friday – that’ll be all the bends I get! My husband will be 59 this year, so we’re getting closer to SS being a decision we’ll have to make. We need to do a lot more research in the next couple of years and posts like this are being bookmarked for that purpose. Thanks for sharing and I’m looking forward to the comments here.

I’m somewhat surprised you haven’t hit the second bend point, but with an educator’s pension, you guys should be in great shape, regardless.

In general, delaying will give you the largest benefit unless you don’t expect to live long after 70. If a spouse is going to take the 50% spousal benefit (not your case), it can become even trickier.

Best,

-PoF