Today’s timely and insightful guest post started as a post in our fatFIRE Facebook group. A generous soul named Mike Magruder, an early retiree in his late forties, shared his actual healthcare expenses from the prior year, along with an outlook for 2020, giving us his true cost of healthcare in early retirement.

Open enrollment via healthcare.gov is underway, and you’ve got about a month to enroll in a plan before the window closes mid-December.

For the first time since I was an independent contractor and locum tenens provider, I am responsible for procuring my own healthcare coverage. I considered alternatives myself, but in the end, I chose a plan from the exchange, just like Mike did.

After reading his post in the group, which was nearly 1,000 words, I sent Mike a friend request and asked if he would mind me sharing his insights with a larger audience. Not only did he oblige, but he more than doubled the length of it by including additional details. More about my new friend:

Mike worked in software development for twenty-eight years in roles including developer, tech lead, architect, and engineering manager. He spent 15 years at Microsoft and more than 4 years at Facebook. He retired in early 2017 at 46 with his lovely wife and two cats in beautiful Washington state where he whiles away the hours volunteering, snowboarding, mountain biking, building snowboards, gardening, and generally goofing off.

The True Cost of Healthcare in Early Retirement: A Guide to Open Enrollment

It’s open enrollment season, so last week I took a close look back at my 2019 healthcare expenses and picked my plan for 2020. I’m going to take you through all of it in detail to help provide a sense of what the costs are for one real couple in early retirement.

My numbers can serve as an example and give you a good starting point to figure out what these costs may be for you. I’ll also add in a few planning suggestions along the way.

Healthcare in early retirement is one of the biggest unknowns for most people planning for FIRE. Whether you’re just starting out or have been on your journey for a decade, no other topic fills us with more dread, uncertainty, and doubt, than how we will get health insurance, how much it will cost, and what it will actually cover.

It’s enough to make a lot of people throw up their hands and decide to work until 65, or seriously consider moving to another country. It feels less predictable than stock market returns. Less transparent than taxes. It feels like you just have to guess.

Part of the problem is that most of us have minimal exposure to the actual cost of health insurance, or to what’s paid when we go to the doctor. Our employers typically cover most or all of our insurance costs, and the entire system does a pretty good job of insulating us from the actual cost of care along the way. There’s no price list when you seek care, and even if you ask the answer is rarely clear until the bill shows up.

I mean, when you have good insurance, who looks at the bill? I know I didn’t. For 20 years, working at places like Microsoft and Facebook, I had what seemed like a magic card I would whip out at the doctor’s office and they’d treat me like a king. I paid little or nothing out of pocket, and I just tossed the statements in the shredder.

Despite all of this, it is possible to plan for these costs in retirement and it doesn’t have to derail you! It feels unknowable, but it’s not. You have to make a projection based on good data just like every other variable in your FIRE planning.

A Little Personal Background

Healthcare is personal. We’re all different, and what I need each year is going to be different from what you need. Age and location also matter greatly. So to put our spending and plans in perspective, you need to know a little about my wife and me.

We’re a married couple, ages 48 and 49, no kids, and non-smokers. We live in King County, WA, (i.e., near Seattle) and have been retired for over 2.5 years.

We each have pre-existing, chronic conditions that require management throughout the year in addition to the normal physicals, flu vaccines, and the occasional laceration.

I have a congenital heart defect and my cardiologist has moved me up to annual monitoring. My wife lost her thyroid to cancer a few years ago and has other issues that require a number of prescriptions and regular doctor visits throughout each year.

Alright, let’s get down to the details!

Our Healthcare Costs in 2019

Our healthcare costs so far for 2019 using Premera Blue Cross PersonalCare Silver, obtained through the WA state healthcare exchange, i.e. the ACA or “Obamacare”:

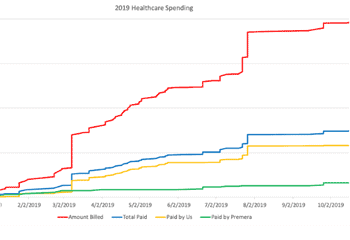

- Amount billed (all doctors, labs, drugs, etc.): $19,634.88

- Discounts for in-network providers: $12,189.68

- Amount paid by Premera: $1,633.13

- We paid: $5,812.07

Neither of us hit our annual deductible of $4,500. I came closest; I think I might be losing a bet with my wife right now.

So, yeah, you’re reading that right. We incurred $19k of medical bills this year. Not premiums, that’s separate. How?!

Well, let’s look at our big expenses:

- My wife’s ongoing ‘mislaid thyroid’ treatment. One example is a generic prescription with a monthly cost that has fluctuated between $77.15 and $170.76 throughout the year. Office visits and three sets of labs ran about $2,388.

- I get an annual echo and cardiologist visit which this year was billed at $1,596.00.

- I messed up my shoulder – torn rotator cuff and SLAP tear – which resulted in 4 doctor visits, X-rays, MRI w/ contrast injection, and some weeks of PT. That MRI alone was billed at $3,814, and the billed costs for the PT were genuinely ludicrous. Imagine if I’d have opted for the shoulder surgery.

- One emergency room trip billed at $2,594.72.

Plus other office visits and prescriptions, the normal preventative care, etc. It adds up fast, and costs are obviously outrageous. Do note, though, the massive difference between billed cost and what is actually paid. I’ve listed the billed amounts to illustrate how we got up to $19k, but we paid much less out-of-pocket.

Charting this is helpful, and you can see some of the bigger events easily.

Of course, that’s just the costs for doctors, labs, drugs, etc. There’s also the actual cost of the insurance plan for the year:

- Insurance Premiums Paid: $15,613.32 ($1,301.11/mo)

So that’s a grand total of $21,425.39 paid by us for healthcare in 2019. (Premiums + “we paid” from above.) A small, nice, new car. A 2020 Subaru Impreza 5-door, base model with automatic, red, prices out at $21,395, so I guess some floor mats are in order.

Gathering the 2019 data

Tracking your true healthcare costs is the first step to getting a handle on this stuff. Premera makes it easy, giving me an Excel spreadsheet to download with everything broken down in detail for the year. Look for something similar from your provider, but if yours doesn’t have that available then start saving those statements you usually toss in the trash!

As you gather your costs be sure to record the category of care for each item. Plans cover office visits, prescriptions, labs, emergency, urgent care, etc. all differently. I haven’t shown this for my costs above, it’s just too much detail here, but I do have it and use it when comparing plans and projecting future out-of-pocket costs.

A portion of Premera Blue Cross Preferred Silver EPO 4500 for 2020

You also need to understand the current cost of your health insurance. Ask your employer what the monthly COBRA payment is for this year, though you might want to make it clear you’re not planning to quit. (Or not, have a little fun with it!)

Start with that number, but note that there is a 2% markup for administration fees. Also recognize that you likely won’t get coverage that good on your own.

Our Plan for 2020

We selected Premera Blue Cross Preferred Silver EPO 4500, which is the replacement for our now discontinued silver plan from 2019. We stuck with Premera’s network for two specific doctors, though there are cheaper options we might consider in future years when one of them retires.

Our rate for 2019 was $1,301.11 per month, and the 2020 plan will be $1,322.74, an increase of ~1.662%. This is the 3rd most expensive plan on the WA state exchange.

So, $15,872.88 in premiums, plus a projected baseline $1,693.32 of out-of-pocket on the silver plan suggests a minimum 2020 total of $17,566.20.

Projected baseline costs for 2020

Given the data from 2019, I can easily add up our expected recurring exams and prescriptions, and use our out-of-pocket costs for those. Most of these costs are co-pays only on the silver plan we selected, which makes them a flat $30 or $60 fee regardless of what the doctor charges or what the prescription really costs.

The biggest variables are labs and tests which are paid by us before the deductible, then 30% co-insurance afterwards, on this plan. I’ll talk about inflating this each year below.

Monthly insurance premiums since retirement

- $1,198.99 – FB’s Aetna PPO via COBRA for most of 2017

- $1,407.33 – FB’s Aetna PPO via COBRA for 2018

- $1,292.60 – Premera Blue Cross PersonalCare Silver for Dec 2018

- $1,301.11 – Premera Blue Cross PersonalCare Silver for 2019

- $1,322.74 – Premera Blue Cross Preferred Silver EPO 4500 for 2020

Why not an HSA plan?

We seriously considered the bronze HSA plan. The premium cost for the HSA plan would have been ~$3k/yr less, and the tax deduction for HSA contributions would have netted us ~$1.5k, but that’s mostly offset for us by the differences in coverage for drugs, urgent care, and office visits.

So it turned out to be mostly a wash with the HSA plan a little ahead, but we stuck with Silver since it should better insulate us from any surprising prescription cost increases, which have already been pretty volatile, and has better urgent care coverage.

The Silver and Gold plans tend to win out when you have a lot of expensive prescriptions or many individual office visits, as you’re charged a fixed co-pay and insurance picks up the rest, while a bronze plan will typically be deductible then co-insurance for those things.

And as you can probably tell by this point, that describes us pretty well.

A spike in either of those categories for us easily wipes out multiple years of the advantage we’d otherwise get on a bronze HSA plan.

More predictability in drug prices and increased skill in mountain biking would both motivate me to reconsider the bronze HSA plan in the future.

How About a Non-Exchange Plan?

I looked at the non-exchange plans available in our county, and the one we’ve selected is preferable to all of them. In general, a “silver” non-exchange plan was much more in line with a bronze exchange plan. I’m not sure if that’s a broader trend or just what the few companies offering these in our county are doing. Your mileage will vary.

Isn’t Obamacare subsidized?

Subsidies are based on income, but we earned more than $67,640 last year (400% of the federal poverty level for a family of two) so we don’t get any. And that feels fair to me, honestly.

2020 Market Overview for King County, WA

There are 32 plans available in King County for 2020, including 2 new carriers, which is up a lot from last year. I don’t have the hard data at hand, but I recall ~14 options last year.

There are a number of HSA options. The lowest cost plan is $755.42/mo and the highest is $1,509.61/mo. Overall rates for ACA plans in WA decreased in 2020 by 3.27%, which is a nice surprise.

Play More, Crash More

Plan on more injuries after early retirement. You’ll be more adventurous with your new free time, I assure you.

I’ve been snowboarding for 20 years, but going multiple times per week throughout the winter instead of working increases the risk of injury. Especially in the first few years when you feel newly free, it makes you want to get after it a bit more than usual.

I also took up mountain biking this past spring, and though it really helped with my physical fitness, being a n00b here resulted in a number of minor injuries and some nicely bruised ribs. And I’m positive I haven’t flown over the bars for the last time yet!

More time in the workshop means more opportunity for metal tools to find their way into my body, etc…

Age Matters

Check rate charts for the cost of your plan at your projected retirement age. It will increase with age, at a surprising rate. Above I noted that our 2019 premium was $1,301.11 per month, and the 2020 plan will be $1,322.74, an increase of ~1.662%. Doesn’t sound bad, right? But there’s more to it than that:

- 2019 premium for a couple 47 & 48: $1301.11

- 2020 premium for a couple 47 & 48: $1266.13

- 2020 premium for a couple 48 & 49: $1322.74

Getting one year older increased the cost by 4.471%. Ouch. That outpaces inflation easily, and even outpaces the steeper inflation of healthcare costs.

So, don’t use the cost at your current age if you think you’re 10 years out from retirement.

A portion of Premera’s gold/silver plan rate chart for 2020.

Healthcare Inflation

You’re already considering inflation in your retirement projections, I’m sure. I’d guess you’re using something in the 2-3% range.

But healthcare costs are growing more rapidly. Here’s a starting point from Premera’s 2020 rate filing with WA state:

“The average cost of a [sic] medical and prescription drug services is expected to increase 3.9%, …”

You’ll want to use this, or something similar, to inflate your projected premiums as well as portions of your baseline out-of-pocket projections each year rather than your usual inflation number.

Co-pays will likely remain stable (they’ll nail you for the rest of it via increased premiums), but anything covered as “deductible then co-insurance X%”, etc., should be inflated to get a better estimate. You can find the full filing with that quote by searching here.

Location Matters

At this point, it should be pretty clear that your location, specifically your county, matters when selecting healthcare on the individual market. I keep pointing out that we live in King County, WA, for a reason!

Check out Premera’s individual rate map for WA in 2020. Ouch. That is severely reduced from 2019.

Lifewise has a more encouraging map but consider how a small move across a county line can result in different premiums or no coverage at all. Have Lifewise living in Seattle and want to move across the sound to Bainbridge Island when you retire? Cool, but find a different insurance company.

Use your local exchange to get a starting point for the county you care about. Start at Healthcare.gov. Take a close look at what plans are offered across your state.

Psychological Effects

For as analytical as you might want to be about costs and plan selection, you can’t ignore the psychological effect of these choices on your and your family. The math may suggest one plan, but you might need to pick a different one anyway.

Early retirement is already a big change in your family’s life. There are new stressors you can’t even imagine yet. Picking the lowest cost plan and switching all of your doctors might not phase you, but what about your spouse?

When someone gets hurt, is their new first thought “How much will this cost? Should we even go to the doctor?” followed closely by “I didn’t have to worry about that before all this FIRE crap.”

It might be worth budgeting a couple grand more per year for a better insurance plan and walking the earth a bit more carefree as a result.

This is the main reason I did the full 18 months of COBRA. Full stability in healthcare; our cards didn’t even change. Well, laziness was a factor too. Retiring is supposed to be fun, and who wants to think about all of this then?

Conclusion

Phew, that was long! It’s a complex topic, with a lot of variables, but again I firmly believe this is something you can get a handle on and plan well. Will your projections be a little off? Sure. But that’s true for quite a lot of retirement planning, and it shouldn’t stop you from forming a good projection and keeping it up-to-date as you approach your goals.

Good luck!

How much are you paying for healthcare coverage in 2019? Do you expect to pay more in 2020? Have you found alternatives to exchange plans to be a viable option for you and your family?

53 thoughts on “The True Cost of Healthcare in Early Retirement: A Guide to Open Enrollment”

I wonder where my comment is.

So assuming 25k costs for 2 or 40k costs for a family of 4, and also assuming that you want a maximum of 20% of your budget to go to health care, with a 3% safe withdrawal rate, one would need a minimum of $4.2M to retire childless or $6.7M to retire with a small family in investible assets, or call it $5M and $8M total net worth counting equity in your primary residence. Better get to saving! Quite impressive to save up almost 8 figures in your mid 40s, guess I should have worked for FAANG

Would love to see a 2022 update to this post topic, since I am in a similar boat – looks like Premera is up ~19% for 2022 plans and the Bronze Cascade plans now offer some copay protection. Does it still make sense to stay Silver?

Great discussion. All the numbers look very inline with my own experience from the past 12 years of early retirement. I’ve been retired longer than the ACA has been in existence, and have been insured under ACA or ACA-like plans since the start. I have not received a dollar of subsidies throughout my whole retirement. I’ve probably spent over $300k total during these 12 years, and my family of 3 has not had any major health issues yet (knock on wood).

I live in a HCOL area (SF), so making 400% FPL is pretty much a given to maintain a basic lifestyle. If you make $1 over 400% FPL, health care costs can be about 25%-40% of your budget, leaving you not much left for other costs. After 12 years, unpredictable health care costs are still my biggest concern. To me depending on continued subsidies would be kind of crimp on retirement mindset.

62 yo retired family doc in Wisconsin, unlucky to have mammogram which revealed breast cancer 2 weeks after retirement, lucky that it was early stage with good prognosis.

Last 12 months, I’ve paid ~$12,000 in premiums (COBRA in 2018, off exchange ACA HSA bronze in 2019), billed medical costs were $398,000, insurance paid $183,000, I paid $9000 out of pocket ($2500 OOPM 2018, $6500 Out of pocket max 2019).

Medical costs can be staggering. It is a relief to have good health insurance when this happens!

I have been a consultant for 12 years now but only had to think about medical insurance after my husband also untethered from the office job 3 years ago. We did COBRA first b/c the devil you know…But that was still over $3k per month, just the premium, copays were extra (we’re 40’s, 2 kids). We’re relocating to FL for 2020 and are targeting an HSA plan for $1300 per month and then covering our adult, but under-26 kids under separate plans for them. HSA works for us b/c I never use traditional healthcare — I’m more into natural and alternative so I always just get insurance for catastrophic protection. Spouse uses it more so we’ll ultimately pick the exact plan where he gets the things he uses. Any way you look at it, it’s a mess. It’s easily our single biggest line item!

Excellent post, we just retired this year, we chose a PPO health insurance through open market (not ACA), $1140 per month for the 3 of us. I’m 44, wife 43 and daughter 10. It is HSA compatible and carries a deductible of $6650 per person per year and $13300 per family per year. Everything goes to deductible first including doctors visits, medications, lab, imaging, ER, hospitalizations, etc, after deductible, insurance pays 100% on everything. Therefore out of pocket max is the same as deductible (plus premium). This is sort of catastrophic plan I guess because I’m paying everything until I max out my out of pocket.

Thoughts:

ACA subsidies are based on MAGI. I don’t see how the $24,400 deduction affects this number.

How does paying Healthcare premiums reduce what I pay to FICA?

Read up on self-pay for laboratory, radiology. There is a local free-standing clinic in my area with prices reduced 90% for these services.

Think twice about Health Care Sharing ministries. My experiment with LHS has been very poor. Quick to collect premiums and no payment. I will likely go on a high deductible ACA Bronze plan after January 1, 2020.

Excellent article and I have owned a small business since 2002 and seen the healthcare premiums costs steadily go up (20-30% for 3-4 years) but this was the first year they stayed roughly the same (2020). My costs for 10K deductible per person for a family of 4 under a HSA High Deductible plan is about 14K + about 3K in actual costs so pretty similar and we are luckily pretty healthy so that is about as low as it could be. As long as it stays 1-5% increase can live with it but if it gets back to 20-30% increases it could get scary very quickly.

On a side note, I have found that paying cash for everything is cheaper than running it through insurance (since I have to pay up to 10K anyways) so it is really catastrophic health coverage. A few years I need a MRI and it would have been 4K if I had ran through health insurance and I paid $500 cash. Did the same thing for my daughters birth (which was not covered under Texas plans)

When I was considering a health sharing ministry as an option, I was prepared to ask for the cash price for everything.

I’ve realized that even with an ACA plan, it’s still a good idea to ask for the cash price versus the insurance price. I’ve heard you can save a lot of money on prescription drugs this way. The cash price may be lower than the copay.

The down side is if you pay cash rather than run the charge through insurance, the out-of-pocket costs will not count towards reaching your deductible.

So many considerations…

Best,

-PoF

I loved reading this detail. I retired in 2019 and went on to COBRA and looked at both the exchange plans for 2020 or converting a small consulting gig for a friend into a remote job with benefits. The remote job won out slightly vs. an exchange plan not due to cost but because the premiums are paid pre-tax with a payroll deduction vs. post-tax with the exchange.

I’m curious if there’s anything in your income you can manage down? Earning a dollar over that income limit costs you around $9,400 when you break just above the 400% of the Federal Poverty Level. That’s a painful cost when we’re all only obligated to pay as much in taxes as we are minimally obligated to do so. That’s a grossly negative return on the last funds earned and I’m confident your lifetime taxes paid are well above what the average citizen pays. You could always voluntarily make a donation to a local human services not for profit to ease your conscience.

I’ve been preparing for a “lunch and learn” retirement talk for our office staff and administrators and this is, of course, one of their biggest concerns. In my reading, it seems that the goal should be to target 100% poverty level with your drawdown plan. Given the standard deduction ($24,000 married), it seems that this should be possible. Based on your calculation of 400% of the poverty line, 100% would be somewhere around $17,000.

So, if you could target having an AGI of $24,000 + $17,000 = $41,000… you get the maximum subsidy, which might save you thousands each year.

Presumably, you could do this if you had a sizeable amount of post-tax accounts (Roth, taxable/brokerage account, etc). You’d need to take out $41,000 from pre-tax accounts and try to take the rest from post-tax accounts.

Is my logic flawed here? If not, this makes for an even better argument to fund your taxable and Roth accounts (And to perform a Roth Ladder conversion in early retirement).

TPP

If you’re retired now with no significant income streams other than those thrown off from or withdrawn from your investment portfolio, I’d say that’s a good plan.

However, if you’re more than a few years from retirement, I wouldn’t count on the ACA and the subsidy formula to be around, so I would not be making investment decisions based on a possible subsidy years down the road.

But your logic based on the current law is not flawed at all. Many early retirees are playing this game as we speak.

Cheers!

-PoF

[edited to remove the reference to the standard deduction that plays no role in the MAGI calculation used to determine subsidies.]

I think the Go Curry Cracker blog talked about this in great detail a few years back. The problem for physicians any way will be your portfolio will likely throw off too much money to use this trick. A first world problem.

TPP, I thought the calculation for MAGI for the purpose of ACA does not include the standard deduction as it’s below the line, i.e., AGI is determined and then the deduction takes place for taxes, not for ACA purposes.

If I’m wrong, I guess I could realize more income this year.

From the IRS:

“For purposes of the premium tax credit, your household income is your modified adjusted gross income plus that of every other member of your family (see question 6) who is required to file a federal income tax return. Modified adjusted gross income is the adjusted gross income on your federal income tax return plus any excluded foreign income, nontaxable Social Security benefits (including tier 1 railroad retirement benefits), and tax-exempt interest received or accrued during the taxable year.”

MedMo, sounds like you are right. The standard/itemized deductions happen after AGI on the tax form.

I think this logic is flawed. ACA subsidies are based on your MAGI, not on your taxable income.

Dan

Great Post. This has been a sticking point for me for the past years. It is hard to determine premiums, co-pays and out of pocket expenses without actually doing it as you did. Having a spouse with an expensive chronic condition and a son with autism really limits my ability to leave the matrix. I found a minor workaround, Semi-retirement. Every single large hospital system or multispecialty group gives access to healthcare to part-time employees in most cases. I recent went part-time and still gets employer-based coverage for a slightly higher premium, ~10%. Not bad so long as I work more than 26 hours a week which is hardly retired.

I recently spoke with a nurse at a competing hospital system who only works one 10hr shift a week and still get access to employer-sponsored insurance. This is amazing since you only need to work 25% of the time to get access to this healthcare. An easy solution would be to work for 1 week a month and still qualify. Not bad if you ask me.

Rock On! Docofalltradez

Very nice and informative perspective. Thank you for sharing.

I’m 61 and bronze ppo HSA $6K deductible plan is $782/month for 2020. That’s with no subsidy.

The premium structure is really a disincentive to working part time when so much of my pay could go to healthcare expenses. At the very least I’m paying $9384 in premiums alone. Currently I get to deduct this against my side business which basically washes out any possible profits and then some.

I live in Florida.

Wow, this is REALLY helpful. We’re still a few years out from retirement, but starting to plan out the possibilities. Healthcare, as always, is one of the big unknowns and the one thing that could keep us working longer than we might otherwise. Thanks to Mike for sharing real information – this helps me build a projection I feel more confident in.

I also want to say I appreciate the section on the ACA subsidies and “…so we don’t get any. And that feels fair to me, honestly.”

Thanks Mike, and PoF!

I’ve glad you enjoyed the post and found it helpful! As a software engineer I love hard data, and sharing it 🙂

It seems ridiculous that we can spend 25k a year, in premiums and out of pocket $,(family of 5, high deductible plan) just to “get” the “discounts” from the insurance, and not meet the deductible…..and the insurance only pays a couple hundred dollars for a child’s well visit and flu shots….

Does anyone know of a catastophic plan out there where we would get ‘cash pay’ rates until we hit 30k of actual medical bills before it kicks in?

We are in our 5th year of insuring ourselves, as husband started own company, and I am an owner in private practice.

Yes, that’s pretty much exactly where we’re at. Nearly $1,000 a month in premiums for what amounts to a catastrophic plan. I didn’t have much luck when trying to find an alternative. If someone has a cheaper catastrophic plan that isn’t full of holes, I’m all ears.

Cheers!

-PoF

It might be fairer if the subsidy was gradually phased out. With the current rules, if income is $1 over the $67,640 “family of two” limit, the entire subsidy is lost. Unexpected mutual fund capital gains can bump income above the limit.

The subsidy cliffs are insane. One dollar of taxable income can cost you thousands of dollars in lost subsidy if it’s the wrong dollar. Why they made it a step-wise progression rather than gradual is beyond me.

Best,

-PoF

Yes, this seems especially horrible given the apparent intent of the subsidies. At the high end, what they’re saying is that you should have to pay more than 10% of your income in healthcare. But fall off the cliff by $1 for a family of 2 and it’s easy for the benchmark silver plan to cost you 20% of your income! Clearly a hole in the plan.

Thanks,

Mike

My least expensive option for my wife and I, both healthy and 63 years old, on the ACA is $1818.86 for a HSA Bronze plan, or $21,826.32 per year added to that is potentially $6,750.00 each as a deductible. So potentially we pay $35,326.32 for healthcare. (The other option costs >$38,000) I retired from Family Medicine and my wife is retired from nursing. I have some deferred comp so I don’t qualify for subsidy. My wife needs her colonoscopy this year along with a Mammogram which should use up her deductible but otherwise we have no medications or health problems. Nonetheless if we get hit by a truck it would jeopardize our entire retirement. >$35,000 just seems excessive. We reside in rrural Wisconsin, so we don’t have many choices.

Scott, ACA plans have to pay 100% for your wife’s annual screening mammogram and for screening colonoscopy, provided that you meet the age and frequency guidelines. I’m 61 and get my checkups and mammogram every year and pay nothing, using my crappy Bronze $6K deductible plan.

I’ve got 22 years before I’m eligible for Medicare, but I’ve ventured into the great unknown regardless. The current system and rate of inflation specifically for healthcare costs is obviously unsustainable.

How or when things will change, I do not know, but if nothing changes, I’d probably be on the hook for $100,000 out-of-pocket in 20 years given the status quo.

Great tip from Lynne on the screening procedures. I’ll be due for the colonoscopy in a little over six years.

Cheers!

-PoF

I was under the impression that those screening tests were covered under most health plans. Maybe it is just in my state.

I also believe Mammos and colonoscopies are covered by ACA plans with no co pay whatsoever. Perhaps you have a “temporary” plan (up to 3 years) which are not ACA compliant but are cheaper.

I have been looking at this issue for years. It has scared me enough to keep working for several years. I am now retired at 62 5/12. I closed my OB/GYN practice at 61. I paid for my own small business blue cross for years. The last premiums at 61 were 650/mo. Lots of co-insurance and surprise fees tho. I then worked for my local hospital for a year with my part of the premium being $180/mo. This was a 3 day/ week job. My contract was not renewed so they had to let me continue on their plan at $180/mo for 3 months. I am negotiating an HR job currently. While negotiations continue my premium is $180/mo. If the job works out…great. If not cobra for $500/mo. If I cobra I am looking at perhaps 12-14 months on either a series of 3 months temp plans at around $900/mo or a Bronze plan at about $1000/month. I am no longer worried because it is pretty finite for me. I will say not working is fantastic and it is easy to injure yourself with all the time to exercise! My knee injury has responded to PT. No copay with the hospital’s insurance. Ha

Thank you for sharing, Hatton1. I’ve enjoyed following your journey as you’ve made this transition over the last several years.

For someone with a net worth at least double ours, you certainly perseverate on the cost of healthcare more than I think is necessary. You cover it like any other cost: pay for it.

Congrats on the retirement, even if it is temporary. An HR job? Am I reading that right — human relations? Hormone replacement? 🙂

Cheers!

-PoF

HR is human resources. Giving talks to students about healthcare careers. The local hospital refers to this as talent aquisition. A perhaps part-time position with a significant benefit.

No kidding? That could be fun and very low risk / low pressure.

Enjoy!

-PoF

We’re scaling back our businesses for 2020 (Coast FI, One More Year, whatever you call it) and will be on a bronze HSA-eligible plan with $0 premiums for a family of three.

Wait a minute.

Those premiums may be fully reimbursed with a tax credit from the federal government, but they’re certainly not $0. Probably in the $600 to $900 range, I would guess.

What’s the cost without factoring in the subsidy?

Best,

-PoF

In the $1500 range for a family of three. Fully reimbursed. In our state the median household income is about $60k/year, and a family of three with an AGI of under about $80k/year gets the full subsidy.

I agree this is confusing. I’m not an expert in ACA subsidies, but for 2020 it appears you are expected to contribute between 2.06% and 9.78% of your income for healthcare costs, based on where you fall between 100% and 400% of the FPL. FPL for a family of 3 is I believe $21,330, so at the lowest end you’re looking at 2.06% * $21,330 = $439.40 per year, or $36-ish per month. Very, very cheap, yes, but not free.

What happens below 100% of the FPL? Is that where Medicaid kicks in and are you talking about being on Medicaid, or is there additional state-specific aid at play here? Would love to know more!

A reference I found, since I was curious: https://www.healthinsurance.org/obamacare/will-you-receive-an-obamacare-premium-subsidy/

Thanks!

Mike – we are in Wyoming and there’s no gradient with subsidies here – it’s all or nothing (not a range of 2.06 to 9.78%, which we did encounter in previous states). We learned this by tinkering around with the marketplace website for our zip code prior to moving here, so the information is there but you have to really dig for it. I’m not sure what happens below the FPL here but our AGI is about 200% of the FPL. Our recent application only indicated the federal tax credit, no state-specific aid.

Ah, Wyoming! Beautiful place, especially Jackson Hole 🙂

And apparently a beautiful place for ACA bronze plans. I found https://www.healthinsurance.org/wyoming-state-health-insurance-exchange/, and more specifically https://www.healthinsurance.org/wyoming-state-health-insurance-exchange/#freebronze. Looks like the cost of your benchmark silver plan is quite outsized vs the bronze. Her examples are pretty interesting, as is this quote:

“The availability of zero-premium plans for middle-class families since 2018 is a result of the cost of CSR being added to silver plan premiums in Wyoming, making premium subsidies much larger relative to the cost of a bronze plan.

And the oddly-priced plans in Wyoming even extend to the gold level. Not counting the three free bronze plans, the three cheapest options available to this family are all gold plans, which are priced below the available silver plan options.”

So that’s pretty awesome!

The article I linked is pretty long, but there is some info in there towards our other question: there’s a gap between Medicaid and 100% FPL in Wyoming that sounds pretty harsh.

PoF – I emailed you a doc with screenshots showing the process. Key takeaways:

-An HSA-eligible high deductible health insurance plan (Bronze) costs $1,496.39/month for a family of three (ages 35, 35 and 6, non-smokers) at full price. $9,000 deductible and $13,500 max out of pocket.

-A modest FIRE AGI of $45,000 qualifies for a tax credit of $1,978/month (more than the premium).

-An AGI of $85,320 qualifies for a tax credit of $1,541/month (still more than the premium).

-An AGI of $85,321 qualifies for zero tax credits.

This means earning one dollar above $85,320 results in paying at least $17,956.68/year in health insurance premiums (and that’s for the lowest cost plan, HDHP). Remember, the median household income in WY is about $60,000 so it’s that generous for the average household, not just lower income early retirees.

Excellent post and thank you for going through it in detail. It is nice to hear from someone who has actually done it rather than someone theorizing about it.

Healthcare is the biggest wild card for me and something that as you pointed out is outpacing inflation with no end in site.

It is amazing what you got charged for the MRI. I don’t have the numbers off the top of my head but I think getting an MRI read at my facility would be maybe 1/4 to 1/5 of that. There is a lot of variability between settings and because there is no price transparency patients really don’t know what the true cost is.

The time between early retirment and qualifying for Medicare is the true danger zone. I will probably try to decrease it by trying to transition to part time first where I still qualify for employer subsidies. But at one point I will have to take it on my own

Our medical system is long overdue for price transparency. Charges should reflect expected payment more closely. The MRI is just a small piece of it, but it’s a big problem.

Best,

-PoF

There were some price transparency requirements for over 300 “shoppable services” in the 2020 OPPS proposed rule in July from CMS, but they got 1,500 comments on this piece of the rule and it looks like it was delayed in the final version that was released last week so they can respond. Hospitals are really pushing back but it is just a matter of time before we see some relief here.

Where’s your facility? I’m moving there… 😀

In 2019, my employer-sponsored HDHP family plan will run $21,564. I will pay about ($4,800) 22% by the end of the year. I get to shelter my piece of the premiums from FICA taxes though which is a pretty nice subsidy. Our deductible is $3,300 with a Max out-of-pocket $6,600. What is your Max out-of-pocket on these plans?

We have not used my health insurance at all with the exception of my annual preventive exam that will run about $200 (they pay that in full). I also get a free cholesterol test out of the deal. We are the “healthy” part of the actuary table this year, but I know that won’t always be the case.

Max

I didn’t include the details of my plan in today’s guest post, but my max out-of-pocket for our family of four will be just over $25k. Premiums of about $11,500 for the year and a family deductible of $13,800 ($6,900 per individual) with a bronze HSA plan.

Like you, we expect to underutilize the plan big-time. But with kids, you never know.

Best,

-PoF

Thanks for sharing – FYI we are heading down to Ecuador on Saturday, you still on the docket next week? Looking forward to some time off.

Max

Yes! I will see you there.

Cheers!

-PoF

For me on the Premera Silver plan (https://www.premera.com/documents/036990_2020.pdf) the max out-of-pocket per individual is $7,350 * 2 = $14,700 for the family. It would be ~$30k for us if we reach the family out-of-pocket, which hopefully will be an exceedingly rare event!

I just left my job on November 1 and will be going on a Cobra starting Dec 1. In 2020 I will pay $700 per month for Cobra just for myself. It would be over $1,600 per month if I included my better half. She is getting a one month short term plan in Dec and will go on the exchange in 2020. I have built a model to figure out the cost of the roughly 60 plans in our area. It was a painful process but well worth the time. When my 18 months of Cobra are up in mid-2021 I will join her on the exchange plans.

My biggest issue with the ACA plans is the limited networks. As a cancer survivor, my oncologist is not in any of the plans. I plan to stay with my specialist so come 2021 I have budgeted the full cost of my 2 semi-annual checkups.

I think by 2023 I have us close to $30k in annual medical costs (premiums and actual expenses). This assumes I hit my out of pocket max each year, I visit my out of network specialist twice a year, and we don’t receive any subsidies. I believe we will get subsidies and I don’t think we will hit the OOPM, but I wanted to build in a worse case scenario too make sure the budget can handle it.

Really enjoyed this piece and seeing that I am not the only one that has spent a lot of time running the numbers!