Hopefully, by the time you are ready to retire, you’re aware of the potential pitfalls and how to handle them. Life can throw curveballs, though, so it’s best to be prepared for both the expected changes and have a plan to take on the unexpected challenges.

Dr. James Dahle highlights the three biggest issues that the retired investor will face. I addressed them in my life preemptively by working “one more year” several times and oversaving for retirement. How will you handle them?

This post was originally published on The White Coat Investor.

Investing in Retirement: The 3 Big Issues

I am often asked about how someone should invest in retirement. My first reaction is usually to wonder why they’re so worried about it. Just as investing for physicians is 95% the same as investing for everyone else, investing in retirement is 95% the same as investing before retirement.

It seems to me that if you can figure out how to stash away enough money to retire on, then it shouldn’t be that hard to figure out how to keep investing that money. However, there are few unique issues unique to retirees that are worth discussing.

#1 Sequence of Returns

The first thing that needs to be understood about investing in retirement is the sequence of returns issue. Basically, this is the fact that not only do your returns matter, but WHEN you get those returns matters.

Many times, just to keep things simple, we use average returns for an investment over decades when illustrating investing principles like compound interest and when doing financial planning. However, in the real world, and especially with volatile, high-return investments like stocks, returns are very irregular.

Even if you have a solid average return of 8-12% on an investment, if you get a long series of poor returns at a critical time in your personal investing timeline, it can sink your plan. This is why safe withdrawal rate studies come out with numbers in the 4% range, even when the investments historically might have averaged 6-8%.

Dealing with this issue should be one of the biggest focuses in any type of retirement planning. In short, your plan needs to account for the fact that your investments may have terrible returns for 5 or 10 years during the critical time period composed of perhaps 5 years prior to your retirement and 10 years after your retirement.

Strategies for dealing with this sequence of returns issue:

- De-Risk Portfolio: Perhaps the most common is to de-risk the portfolio (ie. a less aggressive asset allocation) during these time periods. Increasing bonds with age is commonplace.

- Increase Stock Allocation Later in Retirement: Wade Pfau has demonstrated that the ideal strategy may actually be to increase your stock allocation later in retirement, but the effect of both strategies is similar — a lower stock allocation during the critical years.

- Buckets of Money and TIPS: Other strategies include a “buckets of money” strategy or a TIPS ladder strategy where you basically have the money you intend to spend during the critical period outside of volatile instruments. Using a pension + SPIA + SS for your basic income needs has a similar effect.

- Adjust as You Go: Finally, many investors use a “adjust as you go” strategy and watch their returns carefully those first few years, adjusting their spending down if the dreaded poor return sequence materializes.

#2 The Big Inflation Monster

Another major factor retirees need to deal with is the dragon of inflation. Far too few investors realize that their “opponent” in investing, both before and after retirement, isn’t other investors or “Wall Street.”

It’s inflation, not inflation as measured by the government CPI, but their own personal rate of inflation.

We all know of a widow living on a “fixed income” that on an after-inflation basis is becoming lower each year. This is less of an issue before retirement, when (hopefully) your income and annual savings is increasing each year with inflation and you have plenty of high-risk, high-return investments that are growing faster than inflation.

Strategies available to deal with inflation:

- Continuing to hold some percentage of risky assets in the portfolio

- Using inflation-adjusted pensions, SPIAs, and Social Security

- Using a higher percentage of inflation-linked bonds on the fixed income side

- Owning your residence, which will hopefully eliminate a big chunk of your expenses that rise with inflation

#3 Withdrawal Rates

I often discuss the concept of a safe withdrawal rate, but that is often while doing a calculation to determine how large your nest egg needs to be for retirement, to give you a number to shoot for. As a retiree, withdrawal rates become much more interesting, since your current lifestyle is dramatically affected by your selected portfolio withdrawal rate.

Pick a rate too high, and you’re likely to run out of money before time. Pick a rate too low, and you may unnecessarily impoverish your lifestyle just to leave more money to your heirs, charity, and possibly even the IRS.

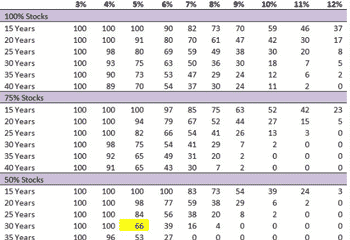

The classic Trinity Study gave us the often-quoted “4% rule” but it is important to understand where that rule came from and what it means.

Basically, using HISTORICAL data (and the future may not resemble the past, especially given our very low interest rates and higher than average stock and real estate valuations), the authors demonstrated that a 50/50 portfolio of large cap stocks and intermediate government bonds was extremely likely to last throughout your retirement if you only took 4%, adjusted to inflation, out each year.

Here’s a copy of that data updated throughout 2009, pilfered from Wade Pfau’s site.

Updated data looks even better, even just a year or so makes a difference as this table goes through 2010.

Every potential retiree, especially an early retiree, should spend some time staring at these charts. The point of the Trinity Study wasn’t to determine whether a safe withdrawal rate (SWR) was 3.5% or 4.5% or 4%, but to demonstrate that it wasn’t the 6%, 8%, or 10% that many investors and planners were using up until that time.

It is also important to understand the concept best shown in this chart:

This shows where the “4% SWR” comes from, i.e. a period of time between 1960 and 1975. Basically, if your “critical investing time period” included the Great Depression or the stagflation of the 1970s, you better not be taking out more than 4% a year.

However, if your own personal critical investing window was any other time, you may have been just fine taking out 5-6% a year. That might seem like a tiny difference, but on a $2 Million portfolio, that’s the difference between spending $80,000 a year and $120,000 a year, a 50% difference.

In Part 2 of this series, we’ll start dealing with how these three big issues that can dramatically affect investing in retirement.

Also bear in mind that these charts use gross income, and never include taxes OR investment fees.

If you’ve chosen to pay 1/4 of your retirement income as a 1% AUM fee to an advisor, you’re going to need to live on 25% less money in retirement, although Michael Kitces makes a good argument about how a 1% AUM fee really only reduces the Safe Withdrawal Rate by 0.4% rather than 1% per year. That’s still $8000 a year on a $2 Million portfolio, hardly insignificant.

What do you think about these three big issues retirees face? Comment below!

3 thoughts on “Investing in Retirement: The 3 Big Issues”

Interesting article on by Kitces on SORR : https://www.kitces.com/blog/monte-carlo-retirement-projection-probability-success-adjustment-minimum-odds/

Maybe we are worrying too much about inflation and SORR.

Inflation risk is mostly in buying Health Insurance (thanks, Obamacare). We are already exposed to hyperinflation in the Health Insurance Marketplace. This cannot be avoided pre-Medicare as everyone needs to purchase Insurance. Going on Medicare greatly ameliorates this type of inflation risk. Otherwise, mitigate inflation (if and when it shows up) by not buying or buying less of inflated items. This could include cutting food budget (less eating out) or buying cheaper cars. If inflation hangs around long enough, bond rates will start to to move up. TIPS are currently paying negative returns. My Money Market funds are currently paying negative returns after taxes and inflation. Hiding in MMF funds doesn’t help. Your best and safest return is paying down debt.

Delaying taking Soc Security also lowers SORR risk. Your return on investment by delaying is huge. Mike Piper has a great free app for optimizing Soc Security benefits especially for married couples.

If you cannot curtail spending under any circumstance, no one can help. Jim Dahle says if you can’t live on 200K per year, you have a spending problem.

There’s never any mention of living off of dividend income (DGI investing strategy) which is a different philosophy from the traditional stock/bond/living off of a 4% withdrawal rate. I know it’s somewhat controversial but well proven to be reliable and not to be discounted when you dig into the data.

Sarah,

I agree with you, but I think POF is not a fan of dividend investing. I don’t mean to be speaking for him, but based on older posts that is my opinion.

In any case, dividends are a tried and true approach to retirement income. I have started the rotation a few years ahead of my retirement to dividend stocks, REIT’s , etc. , just to get a good feel for the income and volatility, mainly in my tax deferred accounts. I have done a fair bit of private equity real estate funds , so I have a good feel for that income stream, but I actually prefer the stability of well known REIT’s, despite the inherent share price fluctuations. Been burned once by a well known private equity manager who went off on a tangent .

Everyone has their own comfort level and approach. Personally , I’m a dividend and real estate fan.