Skip to content

Skip to content

Being retired shouldn’t mean working for free. Retirement forces you to set the conditions under which your time is offered. The challenge lies in deciding when to charge, when to decline and when to give pro bono help within clear boundaries.

Retiring and claiming Social Security may sound like moves to make at the same time. But a sizable group of people on Social Security continues to work after claiming benefits—and that can have implications for financial plans.

For retirees: The $3,000 Mistake 585,000 Retirees Made Last Year (And the 10-Minute Fix)

In today’s fast-paced world, the pressure to do more, achieve more, and be more in less time has become a pervasive part of modern life — and it’s wearing employees out. This relentless urgency can result in a phenomenon known as “hurry sickness.”

Envy can be sicker than greed. Greed is about wanting more of everything. More money, more status, more power. Envy is about wanting what someone else has. You feel like everything in front of you isn’t enough. You become resentful. Here’s how to stop.

When you stop expecting life to be frictionless, you stop being surprised by normal difficulty. And when you reframe challenges as tests of your steadiness, creativity, or patience, something shifts. The problem doesn’t shrink, but your reaction does… and that’s often enough.

Right now many people are debating why the U.S. housing market is broken. Some blame interest rates. Some blame prices. Some blame zoning laws. While the truth is a mix of all of these factors, there’s one thing that no one seems to agree on—supply. Does the U.S. actually have a housing shortage, or is something else going on?

Cities across the U.S. are grappling with two parallel problems: too much empty office space and not enough housing. Nationally, office vacancy rates reached roughly 20% in 2024, after years of employees working from home. Cities like Washington, D.C., are now betting that by turning vacant offices into homes, one crisis can help solve the other.

What if you won a prize and had to choose between a $3 million house and a $3 million portfolio? Which one would you pick? The money offers you far more flexibility and liquidity. A house comes with property taxes, insurance, maintenance, and upkeep.

The U.S. Dollar Index, which measures the dollar’s value against a basket of developed currencies, slid 8% over the past year—and the list of potential concerns grows longer and longer. None of that implies the dollar will suddenly fall from grace, abandoned in a wave of panic selling.

The U.S. economy grew at an annual rate of 4.4% in the third quarter of 2025. The healthcare industry is the only sector growing.

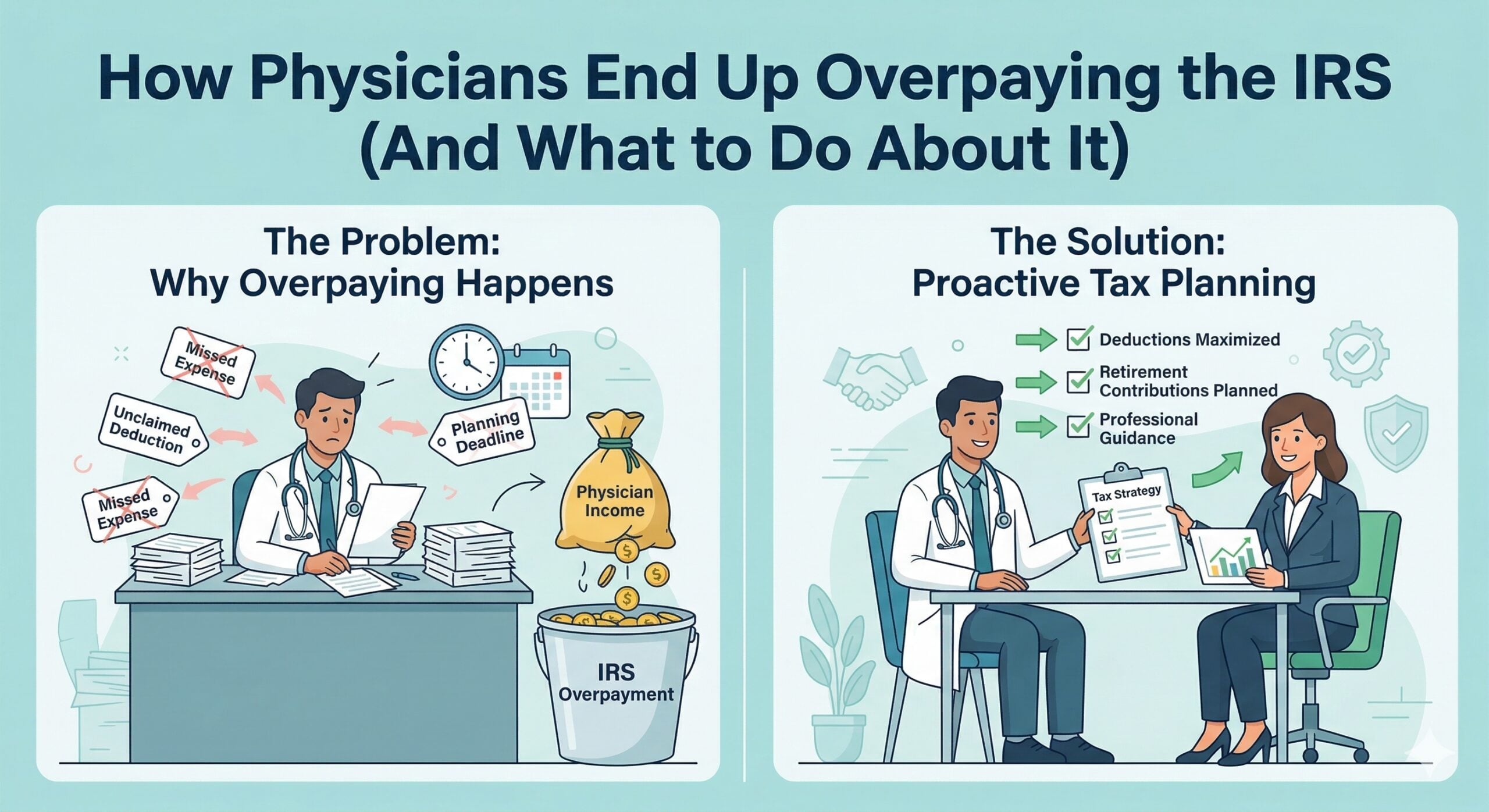

75% of physicians believe they pay too much in taxes. And the data says most of them are right. Here’s where physicians are hemorrhaging money to the IRS.

Americans now spend 10.4% of their disposable income on food. In 1901, it was 42.5%. The long, quiet decline from 42 percent to 10 percent is one of the most consequential economic trends in American history, one that has as much to do with Americans getting richer as it has to do with the price of food.

Legions of fans from around the world have been cheering on Punch, a 7-month-old macaque who had been struggling to socialize at a zoo outside Tokyo.

Your W-2 Is Costing You Money

I paid more in taxes last year than I earned during my entire residency. That sentence still makes me a little queasy.

And here’s what bugs me most: a chunk of that tax bill was avoidable. I just didn’t know it yet.

Most of us got the same financial education in medical school. Zero. So we default to whatever retirement plan our employer hands us, max out the 401(k), maybe fund a backdoor Roth, and call it a day. We assume that’s the whole playbook.

It’s not.

If you’ve ever picked up a moonlighting shift, done any consulting work, or earned a single dollar of 1099 income, you’re sitting on retirement account options that your hospital’s HR department will never mention. Solo 401(k)s. Private-practice retirement structures. Vehicles that let you shelter $69,000 or more per year, legally, while slashing your tax exposure.

I’ve been digging into this topic with Nick Gizzarelli, a Senior Advisor and Retirement Plan Specialist from Earned, and some of what he’s shown me is genuinely frustrating. Not because it’s complicated. Because it’s straightforward, and nobody told us.

We’re cohosting a free webinar on Tuesday, February 24th at 2:30 PM EST / 11:30 AM PST called Beyond the W-2: How Physicians Can Maximize Retirement Contributions Across Income Types.

We’ll cover how even minimal side income unlocks advanced retirement accounts, why your employer plan might be leaving serious money on the table, and the tax mistakes that keep showing up in physician portfolios over and over again.

This one’s worth your lunch break.

[Register here for the free webinar →]

Jorge Sanchez, MD

Naples, Florida

2 thoughts on “The Sunday Best (02/22/26)”

Hello!

Is it possible to listen to the “W-2: How Physicians Can Maximize Retirement Contributions Across Income Types” webinar after the fact? I missed this and very much would have loved to hear all of the great insight. Please let me know if there is a recording available and/or how to gain access.

Thank you!

Reading this feels like a reminder that adulthood is basically a series of expensive default settings — whether it’s claiming Social Security too early, sitting in a high-fee retirement plan, or assuming the housing market “just is what Geometry Dash is.” The real edge seems to be questioning the defaults.