Skip to content

Skip to content

You have people who made life-changing portfolio gains, not from betting against the herd but investing alongside it. Why would you ever sell Nvidia, Bitcoin, Tesla, Facebook, index funds, etc.? Everything that falls immediately goes back up. Don’t fight the trend. Up and to the right.

Car buyers are likely to pay more this fall as tariffs begin to drive up sticker prices — and not just on imported vehicles. Automakers can’t eat the cost of tariffs forever, and September is a convenient time to adjust prices, as the 2026 models begin arriving in showrooms.

Prices of existing homes are still up about 50% from 2019 levels, vs. new single-family homes, which are up less than 30%. Which means that while the July existing home sales report confirmed the ongoing rebalancing of the market, there is still some distance to go.

For the first time in history, it’s cheaper to buy a new home than an existing home. If these conditions continue and further weakening happens, prices will have to change.

The market is filled with intelligent people, but most are constrained by short-term performance metrics. If they have a great business in the portfolio and it lags for 12 months, they risk redemptions, criticism, or even losing their jobs. However, you, as an individual investor, can turn this into your advantage, provided you structure your life so you genuinely can wait.

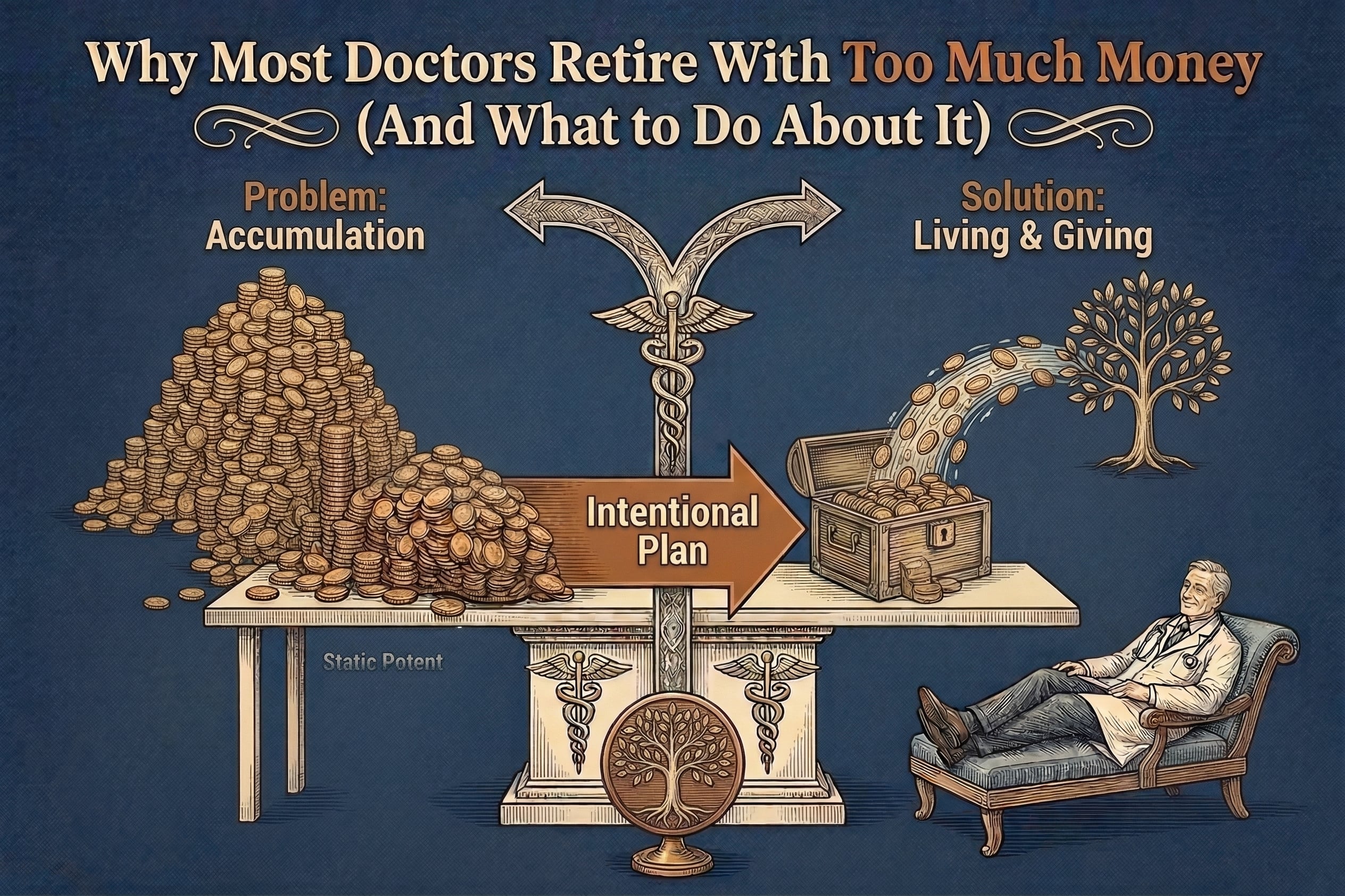

| A 2024 Morningstar study revealed that nearly half of Americans retiring at age 65 could run out of money. That’s a sobering statistic. It’s based on comprehensive simulation data and a host of economic assumptions about Social Security, market returns, savings habits, and more.

But on the other hand, every financial advisor I speak with—especially those working with high-net-worth individuals—shares a wildly different experience. When asked how many of their clients run out of money in retirement, their answer is nearly unanimous: “None.” In fact, many spend a lot of time encouraging clients to spend more. Not less. |

Some of us retire at 70. Others at 40. But no matter your retirement age, your retirement will change over time. No matter your age or retirement plans, the only constant will be change.

According to Pew Research, people aged 75 and older are the fastest-growing segment of the workforce, more than quadrupling in number since 1964. Far from being an anomaly, these seasoned professionals are becoming a strategic asset that forward-thinking employers think they can’t afford to overlook.

If most of your money is trickling down to kids, and if the gift is timed optimally, it can change the trajectory of their lives. A gift that’s less well timed can strain your retirement, create unwanted dependencies, or trigger unnecessary taxes.

How much does it cost to raise a kid in America? The short answer: a lot. The longer answer: somewhere between a new luxury condo and a wrongful-conception jury award.

For Physicians: There’s a core set of deductions that almost every doctor in the United States can take advantage of, regardless of whether you’re working as a hospital-employed W-2 physician, juggling multiple 1099 contracts, or running your private practice.

When Dr. Zeeshan Kharashi, a neuro-radiologist, and his wife Dr. Aswa, a neurologist, looked at their biggest annual expense – their tax bills – they knew something had to change. What happened next transformed not just their financial future, but their entire approach to creating passive income streams that could eventually free them from the demanding schedules of medical practice